Britons could save £300 a month with a “tracker” mortgage as experts predict interest rates will fall in the near future.

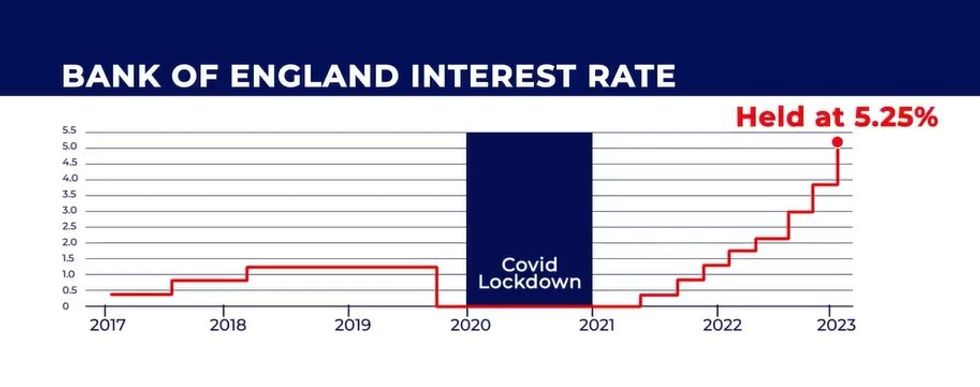

The Bank of England has held the base rate at a 16-year high of 5.25 per cent since August 2024.

While savers have benefited from this decision, mortgage holders and other debt borrowers have experienced skyrocketing costs.

Analysts are betting on the central bank slashing interest rates by as much as 0.25 per cent by June 2024 with further cuts “expected” throughout the year.

What is a “tracker” mortgage?

One of the deals which is being recommended for prospective homebuyers in this environment is a “tracker” or variable mortgage.

This is a type of mortgage which does not have a fixed interest rate attached to it with rates fluctuating depending on the wider market.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

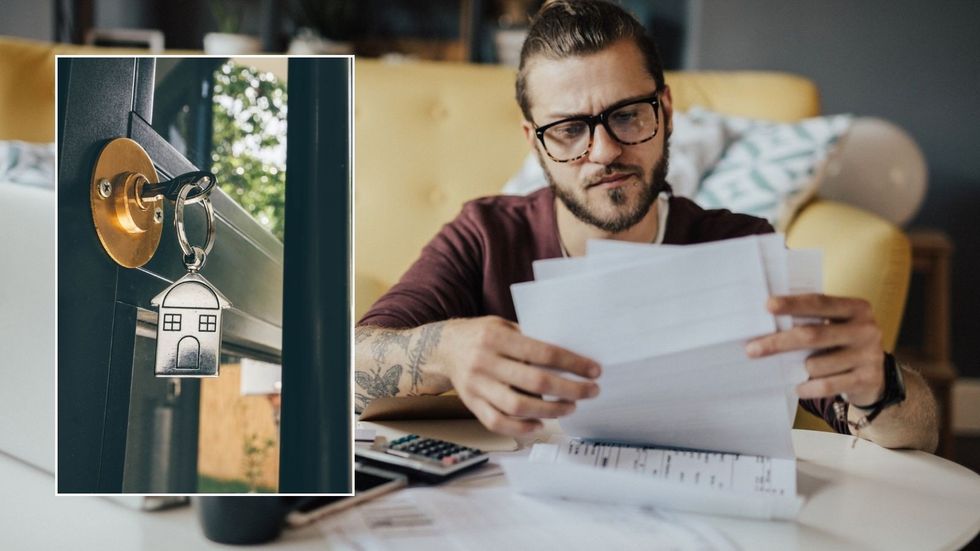

Tracker mortgages could save homeowners money if interest rates come down

|GETTY

A survey carried out by Barrett Developments found that two in three homeowners are aware of this particular loan.

If the base rate were to drop, variable rate mortgages should also fall which would be beneficial for these homeowners’ monthly payments.

Furthermore, certain variable rate mortgages have a cap attached to them which results in interest rates not going above a certain limit, even if the base rate were to rise.

However, if the Bank of England were to announce a surprise rate hike, many variable rates would jump in line with it which could hurt homeowner finances.

Another downside to this deal is that homeowners may not know how much their repayments will be throughout the entire deal period.

On top of this, households might have to pay an early repayment charge if they want to switch before their deal comes to an end.

Adrian MacDiarmid, the head of mortgages at Barratt Developments, outlined why it is important to find the ideal mortgage deal as it could “help save a lot of money”.

He explained: “While a fixed-rate mortgage is the most popular option overall, there are a lot of new products available now tailored to specific buyers.

“The many options available mean that it is always a good idea to take advice from a suitably qualified and regulated mortgage adviser who will be able to help you find the product best suited to your own individual circumstances.

“We have already seen some cuts to mortgage interests at the start of the year and would expect more lenders to follow in the coming days.”

LATEST DEVELOPMENTS:

The Bank of England base rate is at a 15-year high of 5.25 per cent | GB NEWS

The Bank of England base rate is at a 15-year high of 5.25 per cent | GB NEWSThe mortgage expert highlighted that high street lenders are already cutting rates to entice new customers amid a challenging property market.

Mr MacDiarmid added: “Prospective buyers who feared that purchasing their own home was beyond them - because of barriers such as saving for a deposit - could find that mortgages are cheaper than they had expected.”

They might also be able to borrow more than expected by opting for the security of a long-term fixed rate mortgage, which could enable them to borrow up to six times their income.