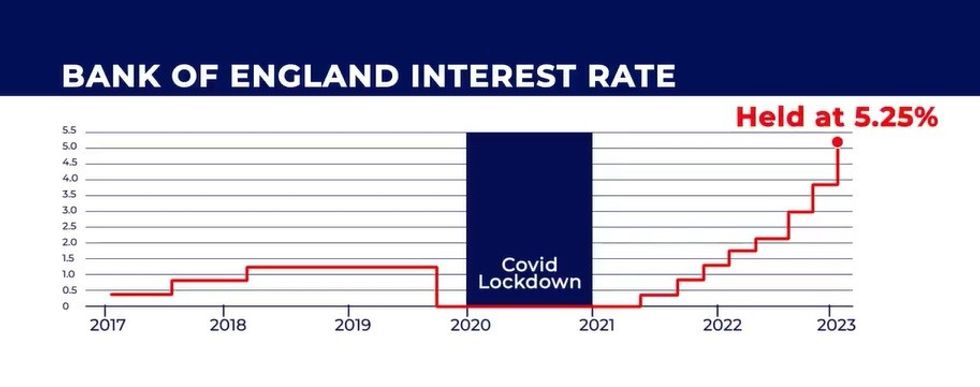

The Bank of England has announced that interest rates will be held at 5.25 per cent for the fifth time in a row.

The Monetary Policy Committee have confirmed that the UK base rate will remain the same and not be cut from its 16 year high.

Bank of England Governor Andrew Bailey said while the economy is “not yet at the point” the base rate can be lowered, things are “moving in the right direction”.

Mr Bailey said: “In recent weeks we’ve seen further encouraging signs that inflation is coming down. We’ve held rates again today at 5.25 per cent because we need to be sure that inflation will fall back to our two per cent target and stay there.

“We’re not yet at the point where we can cut interest rates, but things are moving in the right direction.”

Commenting on the announcement Andy Mielczarek, founder and CEO of SmartSave, said any predictions that yesterday’s data showing a fall in the inflation rate would spark a cut to the base rate was “optimistic”.

He added: “The Bank of England has not bowed to pressure to cut rates in recent months, and it is likely to still be wary of a potential uptick in inflation thanks to tax cuts and minimum wage rising in the coming months.

Interest rates have been raised 14 times in the last year and a half in an attempt to mitigate the impact of inflation on the economy

|GBNews

“Interest rates will come down soon enough, with most experts anticipating a cut in June, or at the latest August. But this won’t mean blue skies all around. While higher interest rates remain a major issue for debtors and mortgage holders, the cost of living is still untenable for many households thanks to slowing wage growth and prices – especially for food – still rising.

“Now is not the time to reduce the base rate; the risk that inflation will rise again is still too great. For those in a position to do so, now is an opportune moment for consumers to take advantage of the available savings opportunities, as we should expect rates to fall as we move closer to the Bank's eventual decision to cut the base rate."

GB News Business and Economics Editor Liam Halligan said: “Inflation did come down but for now the Bank of England are being cautious.

“As long as inflation doesn't surge back we can expect an interest rate cut from the Bank of England very soon.”

With the the MPC voting by a majority of 8–1 to maintain Bank Rate at 5.25 per cent, Mr Halligan said this was a “skewed distribution of votes” when looking at opinion across the city of London.

He continued: “The fact it is eight to one means the first interest rate cut will not be until May or even June when before I could have said April.”UK inflation fell to 3.4 per cent this week, the lowest rate in two and half years, edging closer to the Bank’s two percent target.

Despite the CPI rate of inflation dropping, economists predicted the interest rate would be held at 5.25 percent.

By keeping interest rates high, the Bank is trying to clamp down on the pace of price rises without damaging the economy.CEO of My Community Finance, Tobias Gruber, said: “I must admit feeling a bit disheartened by the Bank of England's decision not to cut interest rates, especially when inflation is creeping closer to the two per cent target faster than anticipated.

“The recent findings from Debt Justice paint a stark reality of Britain's financial landscape, with a record-breaking 6.7 million individuals currently grappling with financial difficulty amidst the escalating cost of living crisis. For the 13 per cent of adults who have missed three or more credit or bill payments in the last six months, a rate cut could have served as a crucial lifeline.”

The fall in the annual inflation rate is due to prices rising less quickly than they were a year ago.

The consumer prices index measure of the cost of living increased by 1.1 per cent in February 2022 but by 0.6 per cent last month.

What it means for your mortgage

Jonathan Bone, mortgage lead at Better.co.uk, suggested those who need to remortgage within the next six months should seek advice from a mortgage broker promptly to assess the available products, including variable rate and tracker mortgages.

While the situation evolves, brokers can provide valuable guidance to help homeowners secure the most suitable deal for their circumstances.

Mr Bone said: “When considering remortgaging, keep in mind that some lenders may charge for valuing your property. If you then spend months weighing up your options and stumble upon a lender offering better rates after a potential Bank of England rate cut, you won't get a refund for that valuation, leaving you out of pocket.

“So, if you're playing the waiting game to see how rates pan out, be aware that not all lenders will charge you a valuation fee and keep your eyes peeled for those offering a free valuation.”

Paresh Raja, CEO of Market Financial Solutions, said: “Mortgage rates have fallen, buyer demand has risen, and we’ve seen a return to growth where house prices are concerned, all contributing to a solid start to the year for the property market.

LATEST DEVELOPMENTS:

“Clearly, buyers are adapting to the higher rate environment, and lenders are being bolder in the rates and products they are offering. This is important - even when the Bank does cut the base rate, we have to be realistic in accepting that rates will not come down as quickly as they went up, so the market has to adjust to a different interest rate environment.

"The early signs are that this is happening, and while inflationary pressures and election uncertainty remain as bumps in the road ahead, there is undoubtedly far greater confidence and optimism permeating through the property market.” However, this does shift the dial for the Bank's May meeting, where we expect to get an update on the timing of rate cuts."

What it means for your savings

Mr Gruber is urging savers to take action. Traditional banks have been sluggish in passing on the benefits of high-interest rates, so it's up to savers to take the reins, he said.

He continued: “Experts are predicting a drop in interest rates by the summer, so seize this opportunity to lock in those top-tier savings rates before they vanish into thin air. Explore your options with credit unions and challenger banks — you might uncover some deals you weren't aware existed.”

Additionally, Will Davies, chief deposits officer at Ford Money said today’s decision provides a “critical opportunity” to secure higher rates of return on their savings, ahead of a potential rate cut later this year.

He said: “This decision comes at a time when inflation rates have fallen to the lowest level in two years, which offers momentary relief for consumers grappling with high living costs, including skyrocketing energy bills, rental expenses, and sluggish wage growth.

“Looking ahead to the coming months, the decrease in inflation will often prompt a cut on interest rates to stimulate economic activity – so, now may be the last chance to capitalise on the current interest rates.”