A former Government minister has warned the state pension triple lock “isn’t forever” amid calls to reform the retirement benefit.

Sir Steve Webb, a partner at Lane, Clark and Peacock (LCP), today told the BBC that the state pension in the UK is “still very low” when compared to other countries.

Under the coalition Government, Sir Steve served as pensions minister and was one of the architects of the state pension as we know it today.

Claimants of the basic and new state pension are being awarded a 8.5 per cent rate hike to their payments from today.

The triple lock pledge guarantees benefit rates will rise every year in line with whichever is highest out of inflation, average earnings or 2.5 per cent.

Rising in line with the average wages element, payments will increase by 8.5 per cent however retirement experts, including Sir Steve, are sounding the alarm over the long-term affordability of the state pension.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

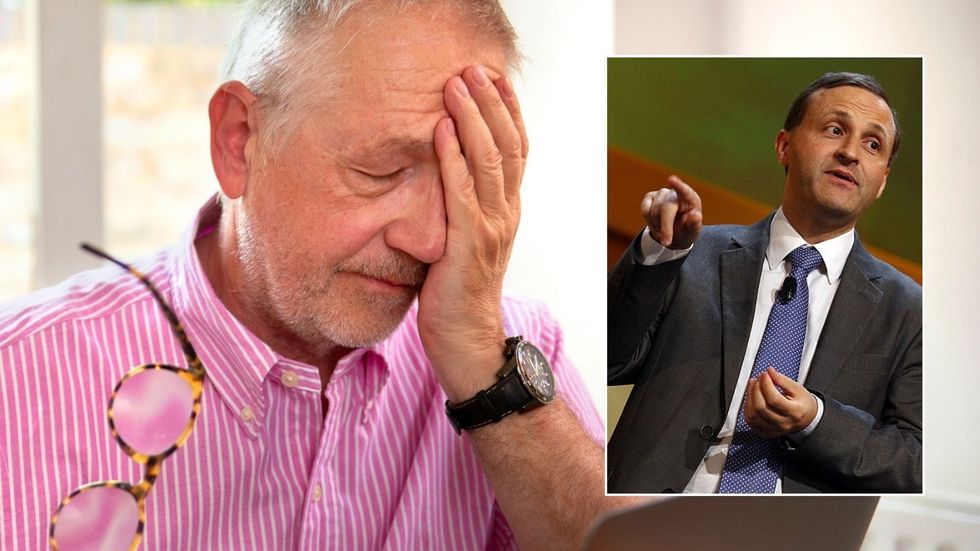

The state pension triple lock "isn't forever", Sir Steve Webb claims

|GETTY

The former Department for Work and Pensions (DWP) minister outlined the reasoning behind the triple lock’s creation and why it may no longer be sustainable going forward.

He explained: “This is a kind of correction going on at the moment. The triple lock isn't forever. It's doing a job of trying to restore the state pension which, by international standards, is still very low.

“The idea of the new system really was to try and simplify things and inevitably you get some rough edges when you do that so we have a new system designed to be ultimately flat rate so people will know what they're going to get.

“It won't vary greatly from person to person and they can plan accordingly. Whereas under the old system, everybody's different.”

According to Sir Steve, the triple lock allowed the pension system to become “more predictable” so retirement savers could plan for their finances.

Research conducted by Standard Life suggests that pensioners are £800 better-off thanks to the triple lock.

If the state pension increased solely in line inflation over the last three years, the full new state pension would only have risen to £10,673.

This is more than £800 less than the full new state pension annual rate, which is now £11,502.40.

Critics have questioned the affordability of the triple lock in the long-term and whether these increases are beneficial for pensioners in light of fiscal drag.

The Government has frozen tax allowances until 2028 which has put many older Britons at risk of being dragged into higher tax brackets as their state pension rises in line with the triple lock.

LATEST DEVELOPMENTS:

Experts are sharing their concerns about the long-term sustainability of the retirement benefit

| GETTYOn this issue, Sir Steve added: “I guess one of the challenges is that for the people on larger pensions they're more likely to be brought into income tax because tax thresholds have been frozen so for those people, 20 per cent could be clawed back by the Government.”

How much is the state pension?

With today’s 8.5 per cent rate hike, the full new state pension has increased from £10,600.20 a year to £11,502.40 from April 2024.

This payment is for those who reached state pension age after April 2016 with claimants eligible for the full amount able to get £221.20 per week.

In comparison, the full basic state pension, for those who became a pensioner before April 2016, is £169.50 weekly. This is represents an increase from £8,122.40 a year to £8,814 annually, for those getting the full amount.