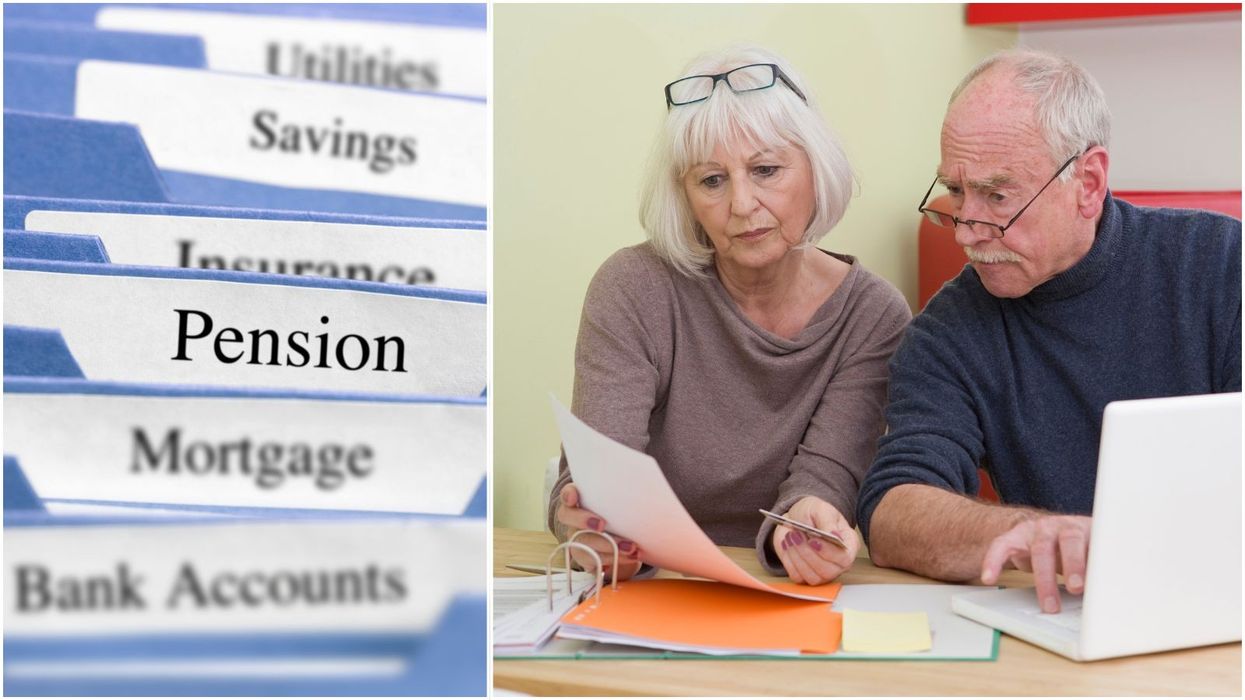

There are six documents that can help alleviate pressures after a loved one has passed away which can facilitate a smooth transfer of wealth.

Having specific documents in place will eliminate family members needing to verify details of the deceased’s assets, accounts and other records that could be crucial for the inheritance tax declaration and winding-up and distribution of the estate.

When planning for later life, it is "crucial" Britons consider the passing of their estate to their loved ones to help eliminate inheritance tax complications as well stress in a hard time.

An expert explained that when a colleague of his passed away, he left a folder on his desk entitled, "‘Dad’s dead – what next!?’"

By having documents in order, his family were able to save time and money trying to sort through his affairs.

Ian Dyall, head of estate planning at Evelyn Partners’ said: "It was an exceptionally thoughtful and useful gift to his family. As an ex-financial adviser, the man was very aware of how stressful administering an estate can be, and that he wouldn’t be around to take care of the family’s financial affairs as he had always previously done.

By having documents in order, his family were able to save time and money trying to sort through his affair

|GETTY

"The folder contained everything his family would need to make the administration process as simple and stress-free as possible, with contact numbers of people who could help.

"This is a relatively simple measure that anyone who is concerned about passing on their wealth smoothly to their family, and making it easier for them, can and probably should adopt."

Dyall shared six key documents families need to spring clean one’s financial affairs for "a smooth transfer of wealth".

Savings, investments, pensions and bank accounts

The estate planning expert explained the document should contain an up-to-date list of one's accounts, what they own and where it is kept such as their investments, debts, bank accounts and professional advisers contact details as well as any debts that they may have such as credit cards, mortgages, car loans as these will need to be repaid before the estate administration can be finalised.

Dyall said: "Think about which past employers hold pension schemes which you belong to and ensure that there are contact details. Whilst you are doing this, take the opportunity to ensure that things pass to the people you want smoothly on death.

"You should nominate beneficiaries for any pension policies or death in service insurance from past employers.

"If you have items that may be difficult to dispose of then you may want to give guidance on how to dispose of them. For example, I have a collection of guitars which would be difficult to value and sell, so I have a list of their approximate values and contact numbers of people I trust who would be able help when selling them."

Paying the inheritance tax bill

Whether mitigating inheritance tax is a priority for someone or not, if there is likely to be an inheritance tax liability on their death then it is worth considering how their executors (someone who is named in the will as responsible for dealing with the estate) will pay it.

Dyall said: "IHT needs to be paid before probate is granted, and probate is required before most companies will release any assets. That is a problem as the executors may not have the funds required to pay the bill.

"The liability on some illiquid assets, including property, can be paid in up to 10 instalments over 10 years, but many executors are forced to borrow money to pay the inheritance tax bill.

"Some assets are accessible prior to probate to pay the bill. National Savings and most banks will pay money directly to HMRC to settle the bill. Also any investments held in trust are controlled by the trustees and are not part of the estate.

"They too can often also be used to pay the liability. Thinking in advance about which assets would be available and whether they would cover the liability can save a lot of administrative hassle and avoid the cost of borrowing to pay the bill."

Wills, trusts and lasting power of attorney

Britons should include a copy of their latest will plus any letter of wishes, their lasting power of attorney (if they have one) and any trusts created with at least two capable trustees.

Records of gifts

Executors will need to know what gifts were made in the seven years before one's death and potentially in the seven years before the earliest of those gifts, in other words up to 14 years before death.

Dyall said: "That is very difficult for an executor to answer unless you have kept a record of the gifts you have made. Records here are especially vital. The tables that need to be completed are in the form IHT403 which can be found on the internet.

"The best approach is to make a copy of the tables required and fill out the form as you go so that there is a rolling record of the gifts made."

LATEST DEVELOPMENTS:

Suppliers and contacts

Details of all the utility suppliers, internet providers, car and house insurance, bank details etc will make it easier to pay the final bills and stop the utilities.

However Britons should be aware that once the bank knows that the account holder has died then the account may be frozen, however many banks will still be prepared to pay the final utility bills, or even release money for the funeral, if they are given proof of the bills.

Dyall added: "My father asked me to help him sort out his own investments recently and we came across details of investments that had long since been encashed. Fortunately, my father was able to tell me which investments were still current, but trying to do that after his death would be much more difficult.

"I would have to contact each provider to work out what happened to those investments, and many of those providers have long since been bought by other providers, so their records aren’t always as good as they could be."

The personal stuff

Dyall explained that discussing difficult topics such as death and funeral arrangements with children can be very beneficial as they will know exactly what you wish for after their death.

He recalled a conversation with his closest colleague that lost her father last year. Dyall said: "He was 90 and had been ill for some time, so he had the opportunity to discuss these difficult topics with her.

"Before his death they had discussed what songs he wanted at the funeral, whether he wanted to be buried or cremated and lots of other issues. She said she found it really helpful emotionally as she didn’t need to agonise over those issues when asked by the funeral directors. She knew she was doing exactly what her dad would have wanted.

"So even if having these discussions in lifetime can seem too difficult, then leaving written instructions will be hugely welcomed by your family."

HM Revenue & Customs pocketed about £700million from inheritance tax last month, this is an increase of £85m from last April.

While only four per cent of estates paid inheritance tax, the most recent figures show, the proportion of deaths resulting in inheritance tax is estimated to grow to over seven per cent by 2032/33.