Pension savers are being urged to “turbo-charge” their retirement pot using the recently announced cut to National Insurance.

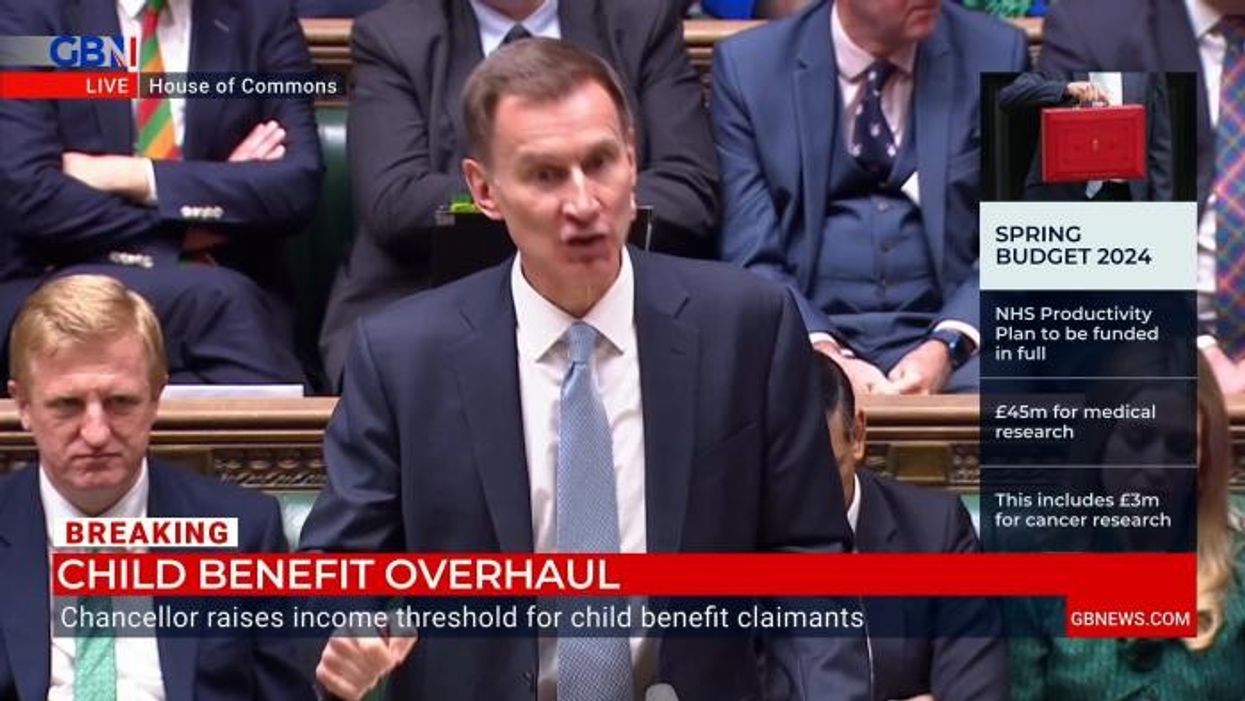

Earlier this week, Chancellor Jeremy Hunt confirmed the levy’s rate for employees will be slashed from 10 per cent to eight per cent, as well as to six per cent for the self-employed, from April.

Combined with the reduction to National Insurance earlier this year, a worker on the average salary will benefit from a £900 boost which could be put towards their pension planning.

However, experts are warning the impact of fiscal drag is diminishing savings made from these tax cuts as Mr Hunt has confirmed tax thresholds will remain frozen until at least 2028.

How will your finances be impacted by Chancellor Jeremy Hunt's Spring Budget? Find out using GB News' 2024 tax calculator here.

Experts are revealing how people can use the National Insurance to to bolster their pension savings

|GETTY

Fiscal drag is used to describe the effect of allowances remaining at the same level over a period of time when wages are rising, resulting in more people paying tax.

Critics have cited the knock-on effect this is having on people’s ability to efficiently save for retirement, especially amid the cost of living crisis.

Lucie Spencer, the financial planning director at Evelyn Partners, reminded those planning for retirement to use this tax cut to their advantage.

She said: “Canny savers can use this latest measure in a way that helps to beat the fiscal drag rise in income tax and turbo-charges their retirement savings – and all without sacrificing take-home pay.

“Given the cost of living pressures everyone has had to endure over the last couple of years, it will hardly be surprising if most earners gratefully pocketed that January cut and let it slide into the current account balance.

“Those whose general financial situation is in decent order – with unsecured debts clear and a cash savings buffer in place - could significantly increase their long-term wealth by simply paying it into their pension, leaving their take-home pay unchanged.”

According to the savings expert, a 25-year-old on the average employed salary of £35,000 could leave themselves nearly £80,000 better off by age 67 through the National Insurance cut.

As well as this, she highlighted how paying into a pension is a useful way of avoiding fiscal drag in the long term.

LATEST DEVELOPMENTS:

Jeremy Hunt outlined his plans for the economy in his Spring Budget | PA

Jeremy Hunt outlined his plans for the economy in his Spring Budget | PA“One of the few ways to mitigate against rising income tax is to pay into a pension, because contributions benefit from tax relief at the earner’s marginal (or highest) rate of income tax,” Ms Spencer added.

“Depending on their pension system, the saver will either get basic rate tax automatically and reclaim the rest if they are a higher or additional rate taxpayer. Or they pay contributions out of gross income and get all tax relief automatically.

“Either way, the effect is much the same: you legitimately avoid paying income tax on a portion of your income while also boosting your pension pot. This is why when someone receives a pay rise, a financial adviser will quite often counsel them to put part or all of it into their pension.”

The cut to National Insurance for employees and self-employed Britons will come into effect from April 2024.