Whether it’s prompted by a New Year’s Resolution, saving up for a big event in 2024 or to build up an emergency fund during cost of living crisis, many will be looking to save money this month.

From the best interest rates to avoiding being unnecessarily taxed on the interest earned, there is a lot to consider with savings.

For those who are looking to build savings pots for the future, savings expert Louise Halliwell, the group savings director at Kent Reliance, has shared some top tips.

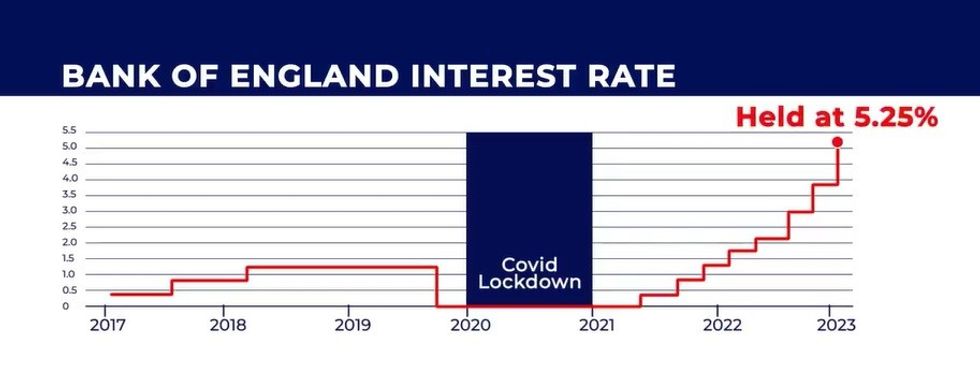

The Bank of England base rate remains at a record high, and as experts speculate about interest rate cuts in 2024, savers are being urged to shop around for the best deals.

The Bank of England base rate is at a 15-year high of 5.25 per cent

|GB NEWS

Ms Halliwell said: “In a year where interest rates are less likely to go up, locking into a good headline rate will be key for savers.

“There are numerous best buy tables that help you find the best rate, so you can make your money work harder and maximise returns.”

When shopping around, the savings expert suggested looking beyond the headline rate.

She said: “Remember the highest interest rate won’t automatically be the best account for you. You should consider other factors, such as whether the interest will be tax-free and how quickly you can access your savings if you need the money.”

Amid a higher interest rate environment, compared to during the coronavirus pandemic, more savers will be at risk of being taxed on their savings interest.

There are ways in which people can legally avoid being unnecessarily taxed, however, such as by making use of ISA wrappers and the personal savings allowance.

Ms Halliwell said: “ISAs often make the headlines as the most tax efficient route for savers - you can save £20,000 a year without paying any tax on the interest you earn.

“However, you can also save tax efficiently through regular savings accounts, using the Personal Savings Allowance - which allows you to earn up to £1,000 in interest (£500 for higher rate taxpayers) before paying tax.”

It’s suggested households protect themselves by building up an emergency fund of at least three months of salary, which could be used to cover any unexpected costs.

Ms Halliwell said: “If something happens with your job or the boiler breaks down, you’ve then got money on hand to help.

“It isn’t easy, but once you get going and get used to reducing a little of your spending money every month, you are more likely to be motivated to continue saving.

LATEST DEVELOPMENTS:

“Once you’ve worked out how much you can save, a good way to get started is to open an easy access savings account where you can put in money and take it out as you need it.

“The rate won’t be as high as if you lock the money away, but it does offer flexibility so you can withdraw your money without facing penalties. “

For money which isn’t needed in case the worst happens, locking money away could mean higher interest rates – although this isn’t always the case, so it’s important to compare the market.

Ms Halliwell said: “You could earn more interest, so what you now need to think about is how long can you afford to not access the money. Typically, terms for notice periods range between 30 and 120 days, although some notice accounts require 180 days.

“Also, think about what kind of saver you are going to be - are you a ‘little and often’ person who wants to put money away every month or do you have a lump sum that you are looking for the best return on?”