Almost £400billion is languishing in UK current and savings accounts which earn one per cent or less in interest, new analysis has found.

Around £380.9billion is estimated to be sitting in current accounts paying between zero to one per cent and instant access non-ISA savings paying 0.01 per cent to one per cent, despite the top easy access account currently paying more than five per cent.

The discrepancy in interest being earned on these savings has sparked a warning for millions of savers making the “costly mistake”.

There are nearly 13 million current accounts held in the UK with balances of £5,001, according to the research from Yorkshire Building Society and data consultancy CACI.

Yorkshire Building Society is warning millions are making a 'costly mistake'

|PA

More than half (55 per cent) of savers have not compared the interest paid on their accounts in the past year, a survey of 2,000 people across the UK for Yorkshire Building Society found.

Nearly half (49 per cent) of people surveyed said they had dipped into their savings in the past 12 months and more than half (53 per cent) said they are happy with their provider.

People said they feel they need easy access to £4,000 on average, the research found.

The average easy access savings rate on the market was 3.16 per cent on Wednesday, according to figures from money comparison website Moneyfacts, while the average one-year fixed savings rate was 4.76 per cent.

Chris Irwin, director of savings at Yorkshire Building Society, said: “Despite savings interest rates getting a lot of attention over the last year, following the significant increases in the (Bank of England base) rate, it’s surprising that there are still large pockets of people who are significantly missing out on savings interest – shopping around can now make a substantial difference to the returns available.

“Keeping large amounts of funds in low-paying current accounts has become a costly mistake for millions.

“It’s understandable to want to have money accessible for emergencies or even topping up everyday expenses, but with so many instant access savings accounts currently available in the market paying a much higher return, there has never been a better time to review the home of your savings.

“Reviewing finances and savings can sometimes be an afterthought, with other things in life taking priority, however, the start of a new year provides the perfect opportunity to take a close look at your finances and increase awareness of your situation and from there look at how you could make small changes which add up to much bigger returns.”

LATEST DEVELOPMENTS:

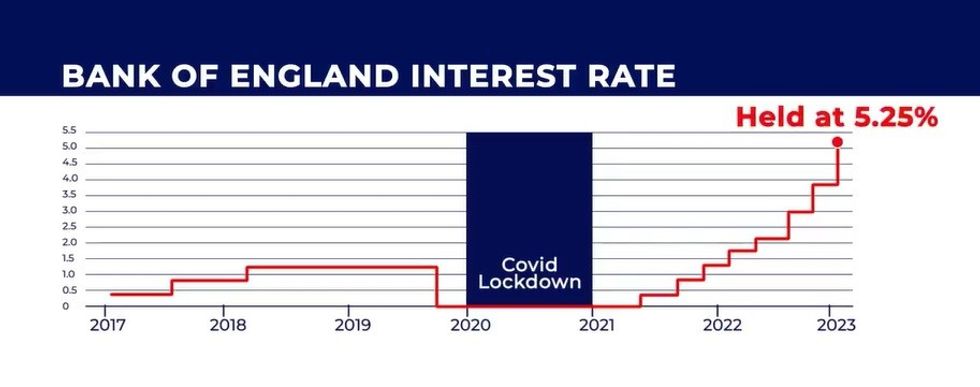

The Bank of England base rate is currently at a 15-year high

|GB NEWS

Rachel Springall, a finance expert at Moneyfactscompare.co.uk said: “Loyalty does not always pay on savings accounts and the convenience of using a current account is costing consumers in interest they could earn elsewhere, as many bank accounts pay little or no interest.”

Interest rates on savings accounts have improved since the coronavirus pandemic when the Bank of England base rate was slashed to just 0.1 per cent.

Savers began to see improvements in the rates they were offered amid the central bank hiking the bank rate 14 consecutive times to 5.25 per cent.

Since raising it to this level, a 15-year high, in August, the Bank of England's Monetary Policy Committee (MPC) has voted to maintain it at this level.