Mortgage rates rose last month amid a “volatile” property market in another blow to homeowners, according to new data.

Experts are warning that interest rates for fixed rate products are going in the “opposite direction borrowers may have hoped”.

Based on figures from Moneyfacts, the average mortgage rates on the overall two- and five-year fixed rate deals rose last month.

This is the reversal of a six-month trend of consecutive cuts to mortgage rates with lenders pricing in a cut to the base rate later in 2024.

The overall average two- and five-year fixed rates increased between the start of February and the start of March, to 5.76 per cent and 5.34 per cent respectively.

Notably, the average two-year fixed mortgage rate stands 0.42 per cent higher than the five-year equivalent.

Do you have a money story you’d like to share? Get in touch by emailing money@gbnews.uk.

Mortgage rates are rising despite an expected rate cut from the Bank of England later in the year

|GETTY

Furthermore, the average “revert to” rate or Standard Variable Rate (SVR) jumped slightly by 0.01 per cent, to 8.18 per cent,

This is just short of the highest recorded rate of 8.19 per cent during November and December 2023, Moneyfacts reports.

Despite these rate hikes, the average two-year tracker variable mortgage continued to be at 6.15 per cent.

In another worrying sign for homeowners, the average shelf-life of a mortgage product plummeted to a six-month low of 15 days which is down from 28 days at the beginning of February 2024.

Rachel Springall, a finance expert at Moneyfacts, described mortgage product availability as “volatile” over the period.

She explained: “Lenders reacted to the change in swap rates, leading to numerous repricing of fixed rate deals, no doubt making it a challenging situation for borrowers and brokers to keep on top of the changes.

“The rate volatility led to a rise in both the overall average two- and five-year fixed rates, the opposite direction borrowers may well have hoped for after positive rate cuts recorded a month prior.

“However, it is worth noting that fixed rates remain lower than at the start of 2024 and there are still some decent options available for borrowers to compare.”

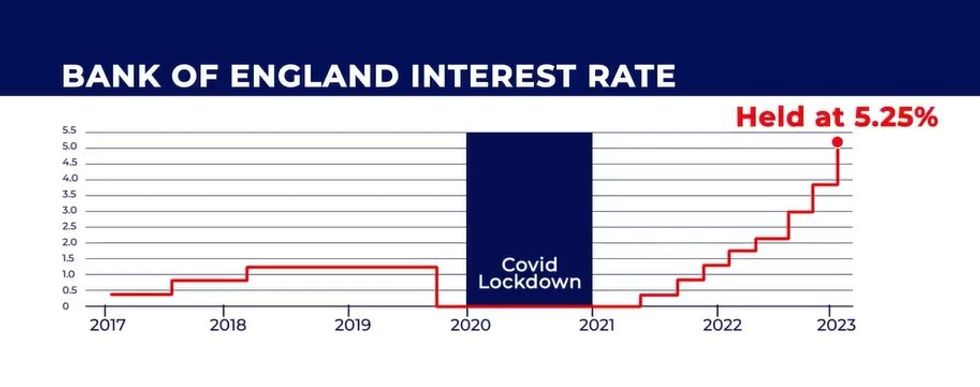

Mortgage rates have remained high over the last 18 months following the Bank of England’s decision to rise the base rate.

The central bank’s Monetary Policy Committee (MPC) hiked interest rates to 5.25 per cent in its fight against inflation.

Analysts are betting on the Bank to cut the base rate later in the year which will likely have an impact on mortgages.

However, concerns have been raised following the recent hike to mortgage rates from high street lenders.

LATEST DEVELOPMENTS:

The Bank of England base rate is at a 15-year high of 5.25 per cent | GB NEWS

The Bank of England base rate is at a 15-year high of 5.25 per cent | GB NEWSMoneyfacts' expert shared advice for Britons who are attempting to get on the property ladder or remortgage despite the state of the market.

Ms Springall added: “As fixed mortgage rates rise, borrowers may wish to wait and see whether these rates will come back down in the weeks to come, but they must keep in mind that there is still an incentive to switch away from a Standard Variable Rate (SVR).

“All eyes are on the Monetary Policy Committee and their future rate setting, in conjunction with the swap rate market, as to whether mortgage rates will come down this year.

“Borrowers would be wise to seek advice if they are looking for a new deal, particularly as the shelf life of a product remains so unpredictable.”