Older Britons can avoid paying tax on their state pension payments thanks to a useful retirement savings hack, analysts are revealing.

A financial strategy enables state pensioners to lawfully bypass taxation on their retirement income while securing an additional £694 annually through pension deferral.

Britons can postpone state pension claims, resulting in a 5.8 per cent enhancement to future payments for each year delayed.

This method proves particularly advantageous for pensioners who continue working, as it prevents their state pension from being subject to income tax while simultaneously increasing their retirement income in subsequent years.

State pensioners could avoid paying tax, analysts warn

|GETTY

The £694 yearly increase continues throughout retirement, potentially creating substantial long-term financial benefits for those who can afford to delay their pension claims.

This mechanism offers dual advantages for employed pensioners who would otherwise surrender portions of their state pension to taxation, creating both immediate tax relief and enhanced future earnings.

While deferring means forgoing pension income during the postponement period, the accumulated yearly increases eventually surpass the initial sacrifice, particularly for those whose pensions would have been taxed.

It should be noted the £694 figure applies to recipients of the full, new state pension, which necessitates approximately 35 years of National Insurance contributions.

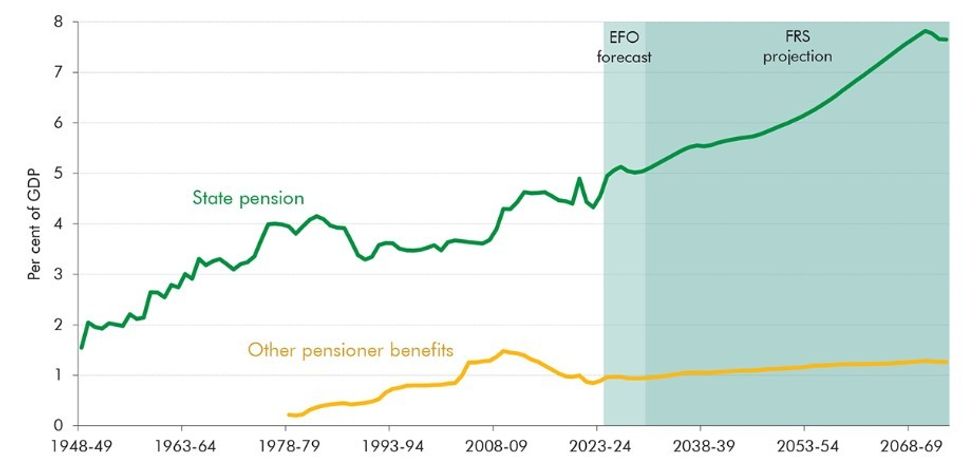

How much will the state pension triple lock cost the British taxpayer? | OBR

How much will the state pension triple lock cost the British taxpayer? | OBR Those with incomplete contribution records would receive proportionally smaller cash increases, though the 5.8 per cent enhancement rate remains constant regardless of pension size.

Financial advisers at Red Dot Group recommend that individuals seeking to optimise their retirement income should undertake a comprehensive review of their financial arrangements.

"To make the most of your retirement, consider reviewing your overall financial plan," the advisers stated.

They suggest beginning with a Government-provided state pension forecast, a complimentary service that reveals projected retirement income and highlights any shortfalls in National Insurance contributions.

"Additionally, explore options like deferring your state pension. For each year you delay claiming it, your payment increases by around 5.8 per cent, which may be valuable for those who can afford to wait," Red Dot Group advised.

In recent months, analysts have warned that the state pension payments are at risk of being taxed as a result of fiscal drag.

This occurs when incomes or inflation rise during a period of time when tax allowances are frozen, resulting in Britons being dragged into higher brackets.

As it stands, the personal savings allowance is set to remain at £12,570 until 2028. This is the amount someone can earn without having to lose money to HM Revenue and Customs (HMRC).

LATEST DEVELOPMENTS:

Fiscal drag is dragging Britons into higher tax brackets | GETTY

Fiscal drag is dragging Britons into higher tax brackets | GETTY Earlier this year, the full new state pension increased by 4.1 per cent to £11,973, with many analysts warning it will likely exceed the tax-free allowance by at least 2027.

David Brooks, the head of policy at pensions consultancy Broadstone, noted more older Britons being forced to contend with income tax is part of the country's "demographic changes due to our ageing population".

He explained: "While perhaps personally frustrating for many pensioners, it reflects the nature of inflation linked occupational pensions and a triple-locked state pension that continue to rise.

"The Government will be called on again to protect pensioners from this impact but with seemingly few ways to control the rise in pensioner incomes, taxation is the only tool left."