Over 700,00 savers are tapping into their pensions before retirement, with over half of these people emptying it completely, new figures have shown.

An increasing number of over 55s have started to draw their pensions entirely as the cost of living continues to bite and they struggle to pay their mortgages and other monthly bills.

Those approaching retirement are warned they face a “very bleak future ahead,” if they are not sensible with their pension withdrawals.

Almost 740,000 pension funds were accessed in the 2022/23 financial year, up around five per cent from the year before, according to new data from the Financial Conduct Authority (FCA).

Some 56 per cent of pots are being cashed in, with the majority of them worth £10,000 or less.

Savers are left feeling desperate for cash as they struggle with high inflation and rising bills.

Paul Leandro, of consultants Barnett Waddingham, said there is a “very bleak future ahead” if people continue to take too much cash too early.

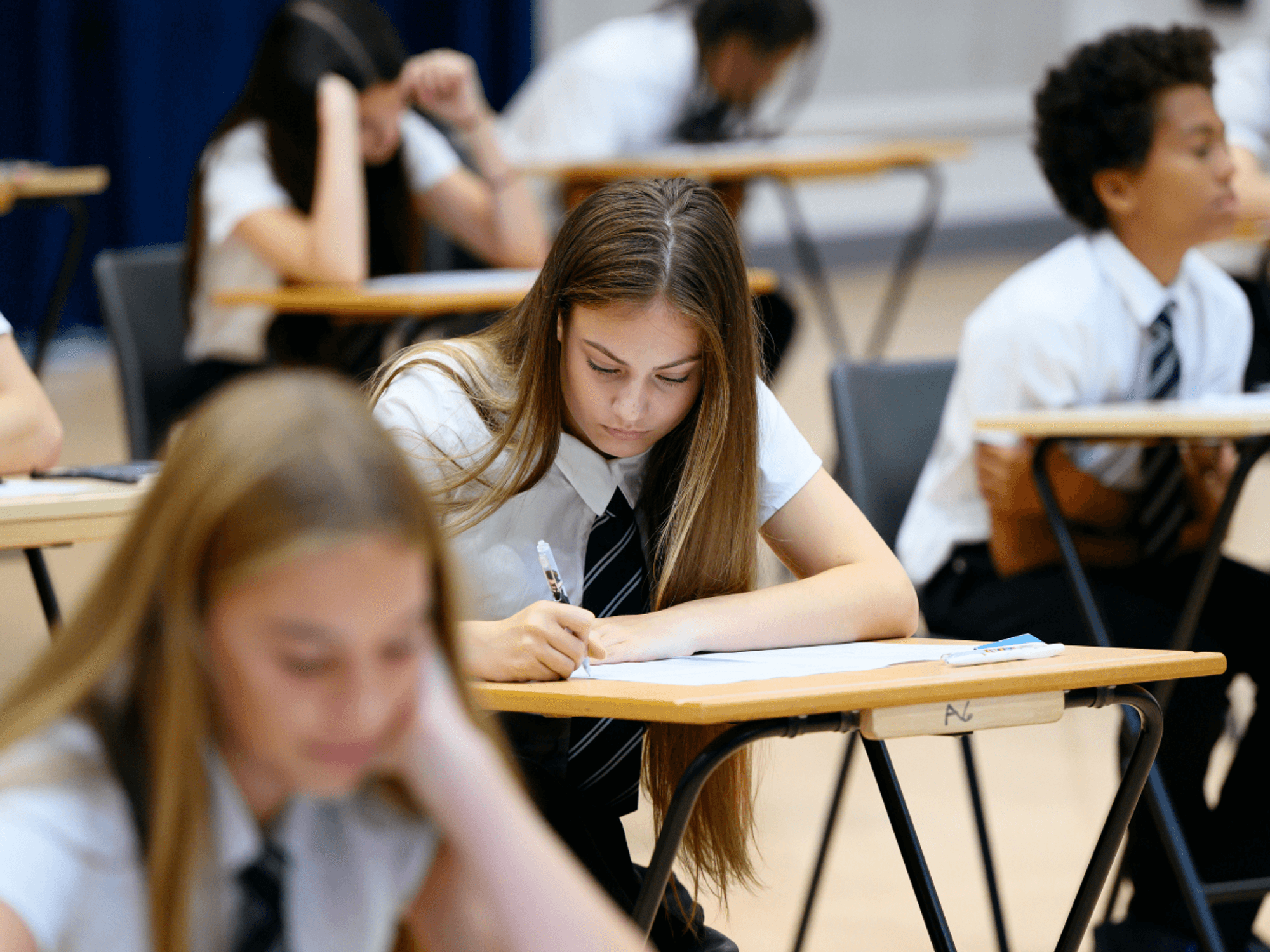

Those approaching retirement could run out of money without careful planning

|GETTY

He said: “The FCA should not be surprised by the increasing levels of cash withdrawals from pension pots, but they should be worried.

“The current pension landscape looks dire. Not enough contributions going in, coupled with too much cash being withdrawn too early, makes for a very bleak future ahead.”

He said pension freedoms introduced by George Osborne 2015, which allowed savers to take a 25per cent tax-free lump sum at the age of 55, opened up “Pandora’s Box”.

Leandro added: “The temptation to draw cash rather than secure retirement income is great, especially in light of the cost-of-living crisis. Some withdrawals may be sensible and financially sound, where the individual has suitable resources, but most are not.

Savers took a record £5.3billion in cash, using three quarters of what they had withdrawn to pay income tax, the report stated.

The FCA found that of the 420,727 pots taken in full, the average was around £12,500. However, tens of thousands took pots worth more than £30,000. This was up from around 395,000 the prior year.

Pension savers are warned withdrawing these high amounts could potentially trigger the Money Purchase Annual Allowance (MPAA).

Exceeding the MPAA means savers could lose tax relief, because they can permanently limit the amount they can contribute in future.

The allowance was £4,000 in 2022-23 but rose to £10,000 last year.

The most common age group for those making total withdrawals was 55- to 64-year-olds, who have not yet reached state pension age, with 294,694 pots accessed.

It was three times those accessed by the next age group, 65- to 74-year-olds, at 114,601.

Steve Webb, former pensions minister and partner at LCP said the findings from the FCA was a demonstration that "hundreds of thousands of people reach retirement each year with very small pension pots".

He said: "These pots would generate very little regular income if spread out over the decades of retirement.”

He suggested that, instead, the majority of people still judge that the best thing to do is to cash out their pension and enjoy some additional cash at the start of their retirement.

Jason Hollands, of Evelyn Partners, said: “One of the factors likely driving higher withdrawals from pensions will be the need to aggressively pay down mortgages.

“For those who took out fixed rate mortgages at the record low rates available a couple of years ago, the prospect of refinancing these with interest rates at the highest level since the 2008 global financial crisis hangs over them like Damocles Sword.

“Some of those tapping into their pension pots to cope with budgetary pressures could be in a position to rebuild their pots with ongoing contributions. But for those who can’t or don’t, early access might raise the spectre of running out of funds later in retirement.”

LATEST DEVELOPMENTS:

As the number of pensioners who can rely on their defined benefit (DB) pensions diminish, Webb argued that we "urgently need to boost pension pots to a size where it makes sense to keep them rather than cash them in".

He added: "With every new set of figures we see the consequences of the government’s delay in expanding automatic enrolment, and the need for urgent action to get Britain saving more for retirement.”

Sales of annuities fell nearly 14 per cent to around 59,200, despite better deals coming on the market as interest rates started to rise.

Similarly, the FCA's new report showed a sharp drop in the number of people transferring out of final salary pensions.

Like annuities, these provide a guaranteed income for life - into invested drawdown plans where the holder bears the investment risk.

However, recent industry figures covering the whole of 2023 suggest more savers are being tempted by a strong recovery in the guaranteed retirement income an annuity will provide.