The head of BlackRock has warned that oil prices rising to $150 per barrel would push the global economy into recession.

Larry Fink, chief executive of BlackRock, said: "If Iran remains a threat and crude prices stay elevated, the consequences for the world economy would be profound."

He said oil prices could fall below pre‑conflict levels if tensions ease and Iran reintegrates into global markets.

However, he warned that a prolonged crisis could result in "years of above $100, closer to $150 oil" leading to "a probably stark and steep recession".

The conflict in the Middle East has increased volatility across financial markets as investors assess the outlook for energy costs.

Britain could face an especially severe economic downturn before the start of 2027, according to analysis from Morgan Stanley.

The investment bank warned the Bank of England may be forced to raise interest rates further if energy prices remain elevated, a move that could push the economy into contraction.

Bruna Skarica, chief UK economist at Morgan Stanley, said: "A pronounced UK recession at the turn of the year" is likely if energy costs remain near recent highs and borrowing costs increase.

Simon French, chief economist at Panmure Liberum, echoed that a recession in the latter half of 2026 "is a real possibility."

Thomas Pugh, chief economist at RSM UK, said: "Everything depends on how energy prices move going forward, but we now expect growth of around 0.5 per cent this year with a decent chance of a recession."

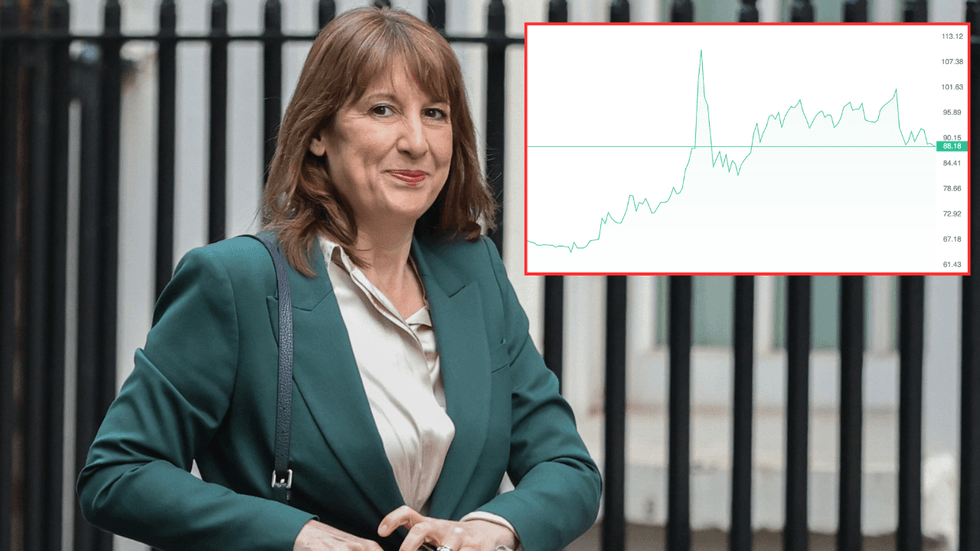

The conflict in the Middle East has massively increased market volatility

|GETTY / TRADING 212

The escalation of conflict involving Iran has driven oil and gas prices higher in recent weeks, increasing pressure on the UK economy.

Manufacturing costs have risen at their fastest rate since September 1992, when sterling was forced out of the European Exchange Rate Mechanism during Black Wednesday.

Data from S&P Global for March showed a sharp increase in factory input prices, reflecting the sector’s reliance on fuel and energy‑intensive materials.

Chris Williamson, chief business economist at S&P Global Market Intelligence, said: "The acceleration in cost growth in the manufacturing sector was especially severe, being the sharpest since the depreciation of sterling following Black Wednesday."

LATEST DEVELOPMENTS

The head of BlackRock warned the impact of sprialling oil prices could be profound on the global economy

|GETTY

He added: "Inflationary pressures have surged higher on the back of rising energy prices and fractured supply chains."

Disruption to shipping through the Strait of Hormuz has reduced fuel supplies, contributing to higher oil and gas prices since the conflict escalated.

Around one in four manufacturers reported longer delivery times from suppliers, with some businesses increasing stock levels to manage potential supply chain disruption.

Private sector activity weakened in March, with the S&P Global composite index falling to 51, its lowest level in six months and only marginally above the threshold for contraction.

Mr Williamson said: "The Middle East conflict has hit the UK economy in March, stalling growth while driving inflation sharply higher."

Business confidence has declined to its lowest level since last June, according to separate data. Retail activity has also fallen sharply, with figures from the Confederation of British Industry showing sales volumes declining as consumers reduce spending.

The drop represents the steepest fall since April 2020, when restrictions during the coronavirus pandemic forced widespread shop closures.

Jake Finney, senior economist at PwC, said: "Private sector growth slowed considerably in March as events in the Middle East clouded the economic outlook, demand has weakened, cost pressures have picked up, and the pace of job cuts has accelerated."

The escalation of conflict involving Iran has driven oil and gas prices higher in recent weeks

|GETTY

Mr Fink said Governments should take a pragmatic approach to energy policy. He said: "Rising energy prices is a very regressive tax. It affects the poor more than the wealthy."

Industry body Offshore Energies UK warned that without increased domestic production, Britain could become more reliant on imports during a period of global instability.

Mr Fink rejected comparisons with the Global Financial Crisis. He said: "I don't see any similarities at all. Zero."

He added that financial institutions are now more resilient than during the banking crisis, and that issues affecting specific funds represent a small part of the wider market.