Analysts are reminding Britons to take advantage of a pension system hack to avoid a "shock" tax raid from HM Revenue and Customs (HMRC).

Millions of workers across the UK who receive pay increases this April could find themselves unexpectedly dragged into the 40 per cent tax bracket, thanks to income tax thresholds that remain frozen until 2031.

An additional 4.8 million people are projected to become higher-rate taxpayers by the end of the freeze period compared to when it commenced in 2022.

Mike Ambery, the retirement Savings Director at Standard Life plc, said: "A pay rise is usually welcome, but it can come as a shock when the increase in take-home pay feels smaller than expected.

Britons are being urged to take advantage of a pension hack to avoid a 'shock' HMRC raid

|GETTY

"That's often because earnings tip more quickly into higher-rate tax than people realise, especially while income tax thresholds remain frozen.

"With millions more people being pulled into higher‑rate tax through no real change in their circumstances, it’s never been more important to understand the tools available to protect your take‑home pay, while staying engaged with your financial future.

"Taking simple, practical steps can help ensure more of your money is working for you - both today and in the years ahead."

The shift coincides with April bill increases, compounding the financial squeeze for affected households. Boosting pension contributions through salary sacrifice represents one of the most straightforward methods for mitigating the impact of crossing into the 40 per cent band.

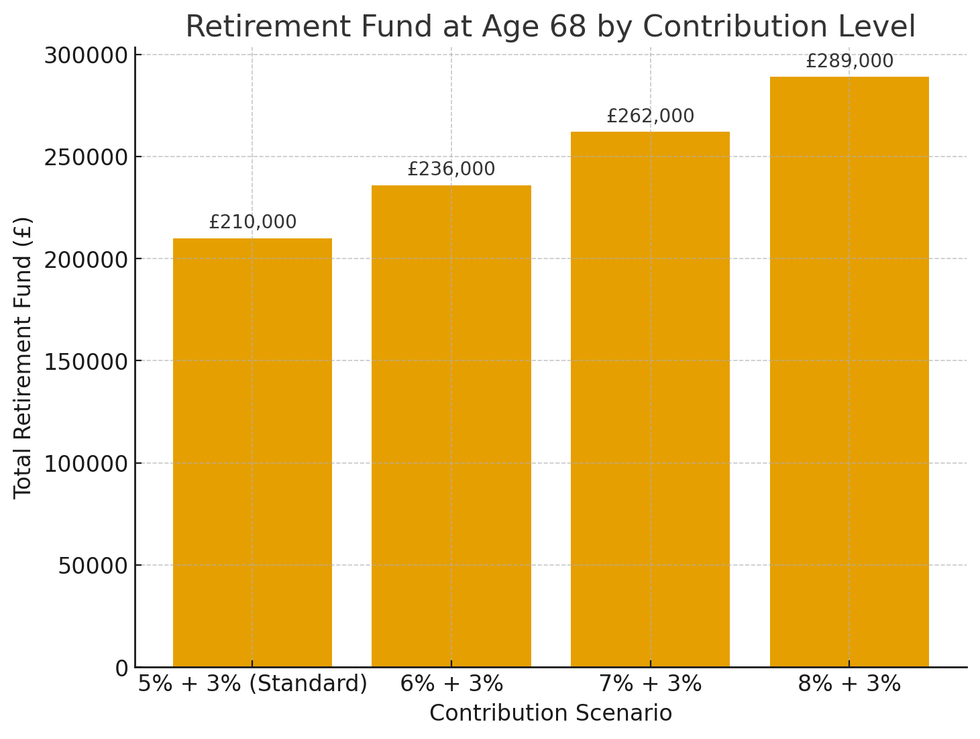

How much can you save towards your pension by making a small sacrifice? | CHAT GPT / STANDARD LIFE

How much can you save towards your pension by making a small sacrifice? | CHAT GPT / STANDARD LIFE LATEST DEVELOPMENTS

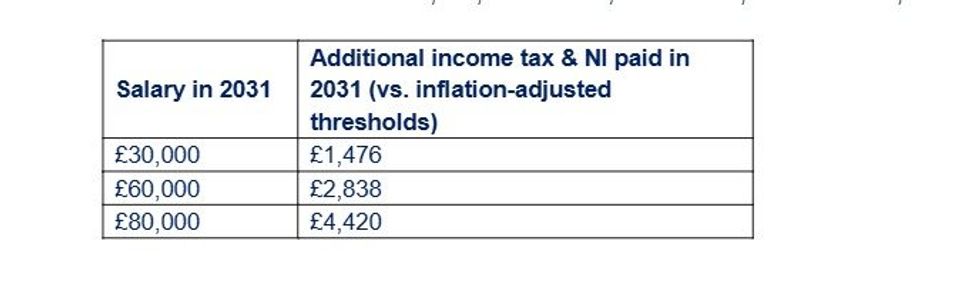

How much more will you pay by 2031 due to fiscal drag? | STANDARD LIFE

How much more will you pay by 2031 due to fiscal drag? | STANDARD LIFEThis allows payments to be made from gross salary, reducing both the amount subject to higher-rate tax and National Insurance obligations simultaneously. Mr Ambery cited the example of a worker on £50,000 who receives a £5,000 increase, pushing their earnings to £55,000.

Of that rise, £4,730 falls above the higher-rate threshold of £50,270 and would ordinarily attract 40 per cent tax plus National Insurance, sending £2,062 to HMRC before accounting for student loan deductions.

Directing the entire £5,000 into a pension via salary sacrifice eliminates the higher-rate liability on that income while cutting National Insurance contributions. Some employers pass on a portion of their own National Insurance savings, further enhancing the pension pot.

The Government intends to alter salary sacrifice regulations from April 2029, restricting the NI exemption to the first £2,000. UK taxpayers receive pension tax relief corresponding to their income tax rate.

How much pension tax relief you can get depends on your earnings | AJ Bell analysis of HMRC data

How much pension tax relief you can get depends on your earnings | AJ Bell analysis of HMRC dataThose on the basic rate benefit from a 20 per cent Government top-up, effectively meaning £100 enters their pension for just £80 of their own money.

Higher-rate taxpayers qualify for an additional 20 per cent relief, bringing total relief to 40 per cent, while those in the additional-rate bracket can claim up to 45 per cent.

However, this extra relief for higher earners is not always applied automatically. Depending on how contributions are structured, individuals may need to reclaim the additional amount directly from HMRC, either through Self Assessment or by contacting the tax authority.

Any relief owed is typically returned as a refund or adjusted through the tax code. Those who have missed claiming in previous years can generally backdate requests for up to four tax years.