A major shift in pension taxation is just over a year away, with changes set to bring unused defined contribution pension savings into the scope of inheritance tax.

From next year, any unused money held in defined contribution pensions will be counted as part of an individual’s estate for inheritance tax purposes.

The change is expected to draw more estates into the inheritance tax net, although the overall proportion of people affected is forecast to remain relatively small.

The reform means some families could face unexpected tax liabilities during bereavement if planning has not been undertaken in advance.

TRENDING

Stories

Videos

Your Say

Inheritance tax becomes payable when an estate exceeds £325,000, known as the nil rate band.

An additional allowance, called the residence nil rate band, provides a further £175,000 when passing a home to children or grandchildren.

Married couples and civil partners can transfer assets to each other without incurring inheritance tax due to the spousal exemption.

They can also inherit any unused nil rate bands, meaning a surviving partner could pass on up to £1million without triggering inheritance tax.

Families face surprise inheritance tax bills under pension rule change

|GETTY

Cohabiting couples are not eligible for the same exemptions under current rules.

Gifting assets is one method individuals may use to reduce the size of their estate ahead of the changes.

There is an annual gifting allowance of £3,000, which can be carried forward by one year if unused.

Larger gifts, known as Potentially Exempt Transfers, fall outside the estate if the individual survives for seven years after making them.

LATEST DEVELOPMENTS

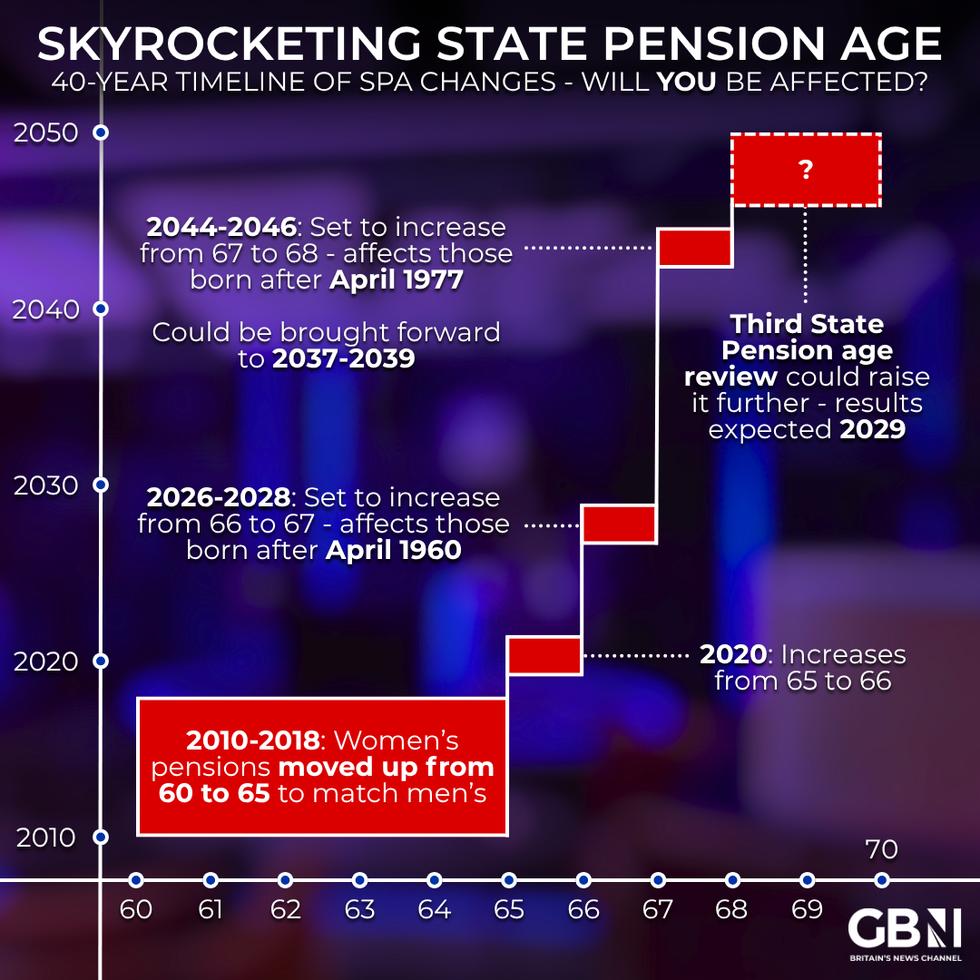

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYIf death occurs within that period, inheritance tax may still apply, although the rate can be reduced depending on timing.

Specific exemptions also apply to wedding gifts, with limits of £5,000 for a child, £2,500 for a grandchild and £1,000 for others.

Individuals may also give away surplus income without affecting their estate, provided the payments do not reduce their standard of living.

Certain conditions apply to ensure gifts are not still considered part of the estate.

For example, assets given away but still used by the original owner, such as continuing to live in a gifted property without paying market rent, may be treated as a "gift with reservation" and remain subject to inheritance tax.

Maintaining records of gifts, particularly those made from surplus income, is required to demonstrate compliance with the rules.

Professional advice may be sought to ensure estate planning aligns with current inheritance tax regulations.

Our Standards: The GB News Editorial Charter