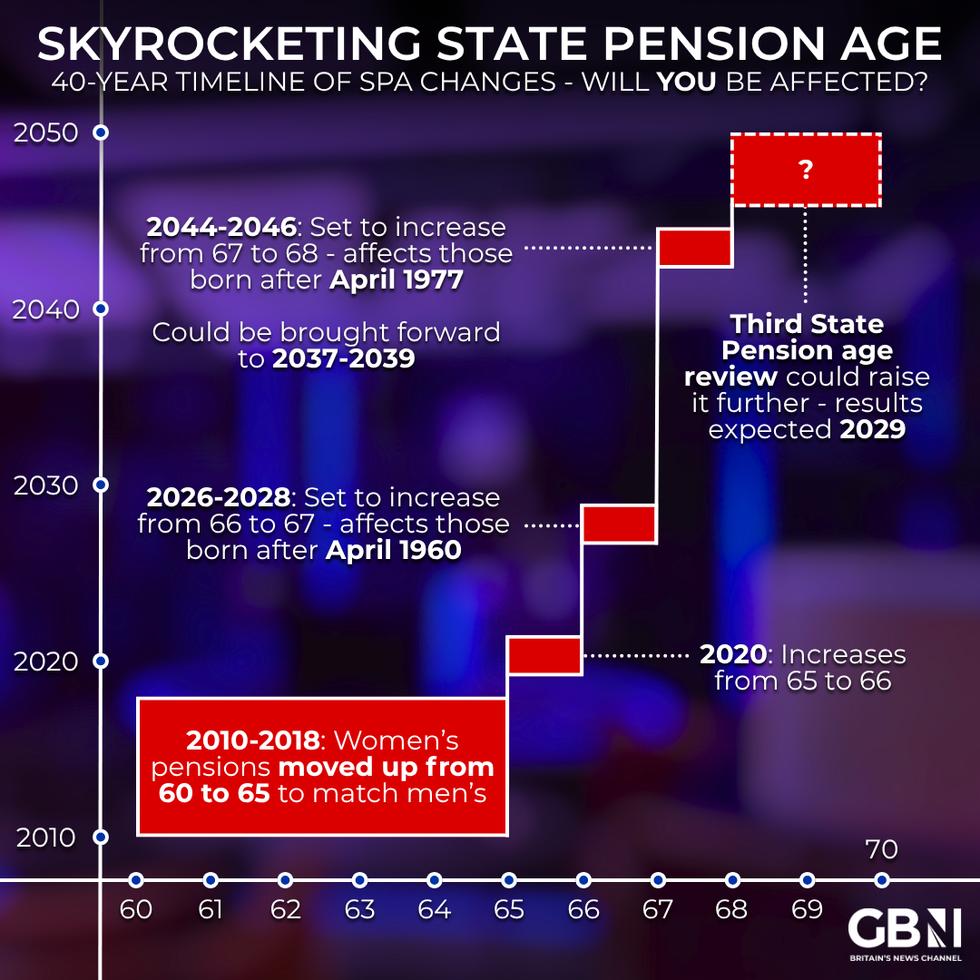

A major state pension age is due to take place from next month, with the retirement age set to gradually increase from 66 to 67, marking a significant shift for millions of people across Britain.

This comes as analysts warn that retirees are set to face being taxed on their state pension alone from next year due to the impact of fiscal drag.

Those born between March 6, 1961, and April 5, 1977 will be affected by this change, becoming eligible to claim their state pension only upon reaching their 67th birthday.

The transition is expected to be fully implemented by 2028. This adjustment has been on the statute books since the Pensions Act 2014, which accelerated the timetable by eight years.

Major changes to the state pension regime are set to take place

|GETTY

Rather than everyone becoming eligible on a single date, the new system ties eligibility directly to an individual's 67th birthday. The Department for Work and Pensions (DWP) will contact all those affected with advance notice of the changes to their retirement date.

For the maximum weekly payment of £230.25 under the new state pension, approximately 35 years of contributions are typically required. However, those who were previously 'contracted out' may need additional years to reach the full amount.

A qualifying year is achieved when someone earns at least a certain threshold while employed, or receives National Insurance credits during periods of unemployment, illness, or while caring for others.

Currently, more than 13 million older people throughout the country receive regular income from the state pension, according to DWP figures. Many approaching retirement may be relying on this contributory benefit as their primary income source.

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYLATEST DEVELOPMENTS

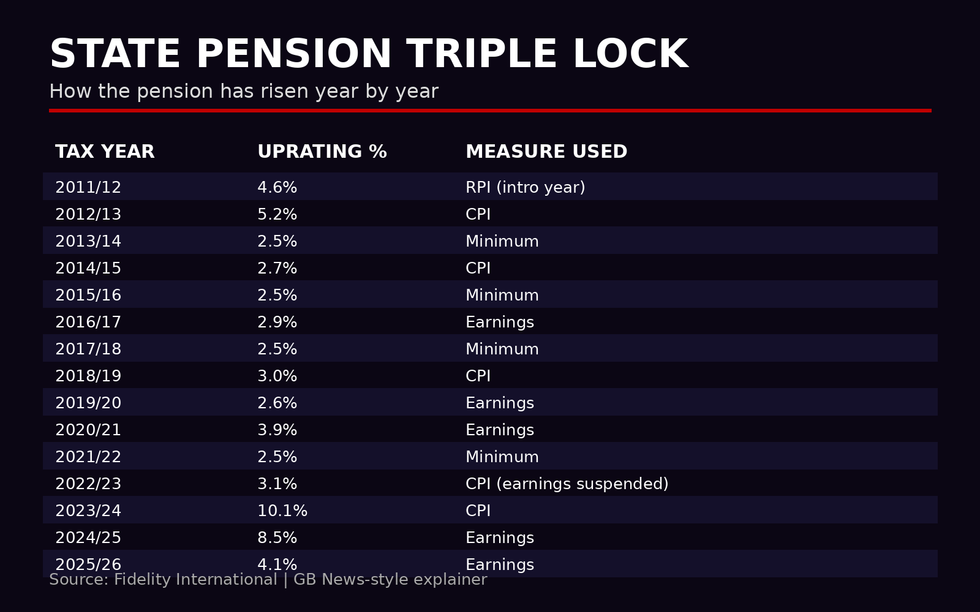

How much has the state pension risen by thanks to the triple lock? | GB NEWS / FIDELITY INTERNATIONAL

How much has the state pension risen by thanks to the triple lock? | GB NEWS / FIDELITY INTERNATIONAL Those wanting to verify their entitlements can access free online tools on the GOV.UK website. A state pension statement will reveal the projected amount someone may receive upon retirement.

Additionally, individuals can request a National Insurance statement from HMRC to identify any gaps in their contribution record. Where gaps exist that would prevent someone from obtaining the full new State Pension, options are available to address this.

It may be possible to pay voluntary contributions to fill missing years, or to claim National Insurance credits for eligible periods. The GOV.UK website also offers a tool to check State Pension age and confirm when someone becomes eligible to claim.

A significant number of people remain unaware of an important tax consideration regarding their State Pension.

Currently, the full new state pension stands at £230.25 weekly | GETTY

Currently, the full new state pension stands at £230.25 weekly | GETTYSarah Pennells, consumer finance specialist at Royal London, said: "The fact that approximately four in 10 adults do not know the state pension is taxable is not surprising as it's paid without tax being taken off.

"However, from April, the full new state pension will be less than £30 below the personal allowance, so it's more important than ever that people understand what tax they may have to pay."

Royal London's research indicates that nearly 68 per cent of retired individuals not in employment paid tax on their pension income, with the average bill exceeding £4,500.

More From GB News