Retirees across the UK are receiving unexpected letters from HM Revenue and Customs (HMRC) after discovering their state pension income may be subject to tax.

Many pensioners had been unaware that the state pension is taxable, as payments are made without tax being deducted at source.

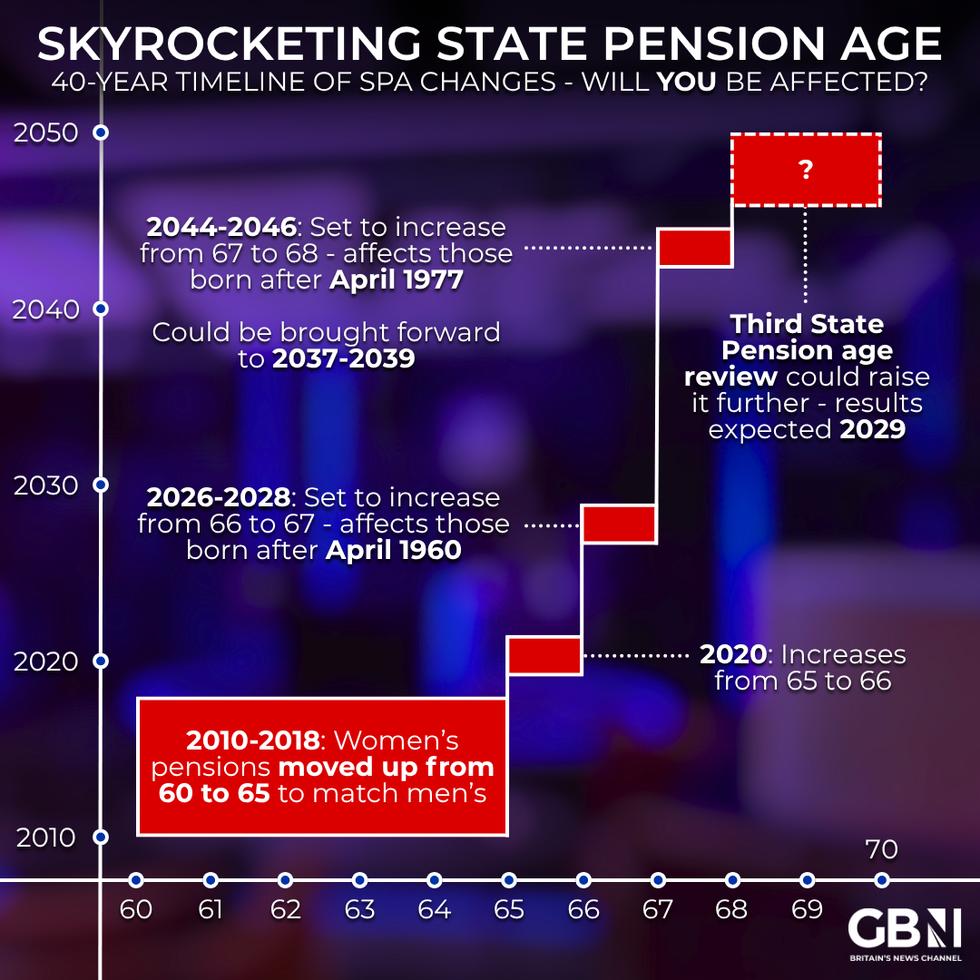

The state pension age currently stands at 66 and is set to begin rising to 67 from April.

The increase will be phased in and completed by 2028.

Those born between March 6, 1961 and April 5, 1977 will need to wait until age 67 before they can claim their state pension.

An increase in payments from April is expected to bring more retirees into the tax system.

The full new state pension will sit just under £30 below the personal allowance threshold, increasing the likelihood that those with additional income will face a tax bill.

Sarah Pennells, consumer finance specialist at Royal London, said: "The fact that approximately four in 10 adults do not know the state pension is taxable is not surprising as it's paid without tax being taken off."

'Four in 10 unaware' as HMRC letters hit retirees over state pension tax

|GETTY

She added: "However, from April, the full new state pension will be less than £30 below the personal allowance, so it's more important than ever that people understand what tax they may have to pay."

The narrow gap between pension income and the tax-free threshold means even modest additional earnings could push retirees into paying tax.

Research from Royal London shows that around 68 per cent of retired people who are not working paid tax on their pension income.

The average annual tax bill for these individuals exceeded £4,500.

LATEST DEVELOPMENTS

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYThe figures highlight the growing financial impact of pension taxation for those in retirement.

The planned increase in the state pension age will affect those born between March 6, 1961, and April 5, 1977, who will only become eligible to claim at age 67.

Ms Pennells said: "With the State Pension age now at 66 and due to start rising to 67 from April, many people are only too keen to claim their State Pension."

Royal London data indicates that the number of people deferring their state pension fell in 2023 to 2024 compared with the previous year.

This trend may reflect the financial pressure on retirees who are less able to delay receiving income.

However, the rise in payments towards the personal allowance threshold could lead some individuals with additional income to consider deferring in order to manage their tax position.

Ms Pennells said: "If you're thinking of delaying claiming your State Pension, then it's a good idea to assess whether it is right for you."

She added: "Getting the extra money may look attractive, but you are giving up the right to receive any State Pension payments until you stop deferring, and it could take years to see the benefit."

She said surviving spouses or civil partners can only inherit additional pension payments if the person who deferred reached state pension age before April 6, 2016.