State pension payments are due to receive an inflation-busting rate increase next month, but analysts are warning that a future tax bill in 2027 "shouldn't go unnoticed".

Retirees will see their income rise by 4.8 per cent when the annual increase takes effect on April 6, delivering a boost that outpaces the current rate of inflation.

The Office for National Statistics (ONS) confirmed that the consumer prices index (CPI) stood at three per cent for the year to February 2026, matching January's figure.

Under the triple lock formula, which bases increases on earnings growth, inflation, or a minimum of 2.5 per cent, this year's uplift was determined by wage growth figures.

State pensioners face a 'tax bill' despite the triple lock boost next month

|GETTY

Recipients of the new state pension will now receive £12,547 per year, an increase of £574 from the previous £11,973 annual amount.

Those on the basic state pension will see their payments climb from £9,175 to £9,614 annually, representing a £439 rise.

Kate Smith, the head of Pensions at Aegon, described the upcoming rise as "a welcome 4.8 per cent boost to their income".

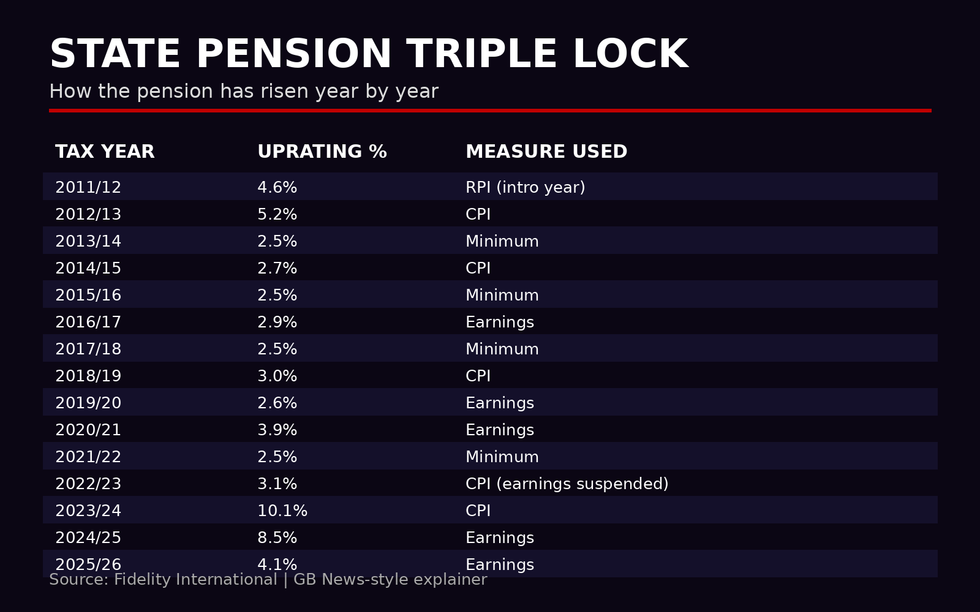

She noted: "This year's increase represents the fourth-highest jump since the triple lock was introduced in 2011, a system whereby the state pension increases annually at whichever is highest out of CPI inflation for September, earnings growth for May to July, or a 2.5 per cent minimum."

How much has the state pension risen by thanks to the triple lock? | GB NEWS / FIDELITY INTERNATIONAL

How much has the state pension risen by thanks to the triple lock? | GB NEWS / FIDELITY INTERNATIONAL LATEST DEVELOPMENTS

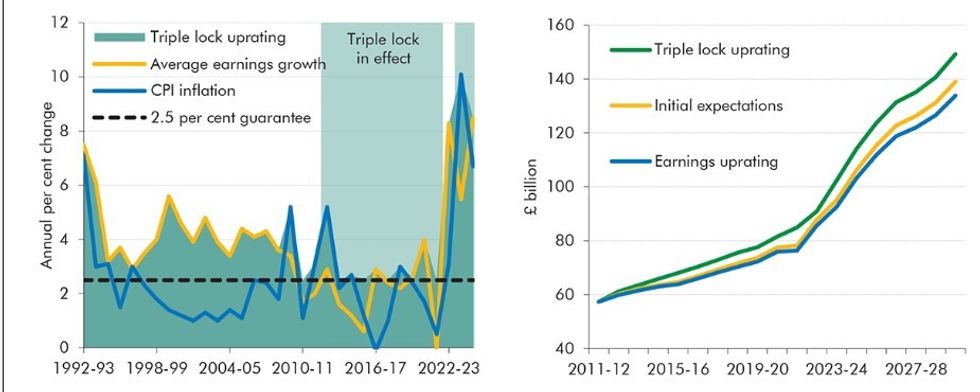

What has the impact of the state pension triple lock been on the public's finances | OBR

What has the impact of the state pension triple lock been on the public's finances | OBR The triple lock mechanism has protected pensioner incomes since its introduction, guaranteeing annual rises based on whichever measure proves most generous.

Ms Smith added: "Given today's announcement that inflation currently sits at three per cent, state pensioners may be particularly pleased to see that their increase is above the rate at which costs are rising, indicating their income may be able to go a little further too."

The new state pension figure of £12,547 now sits perilously close to the income tax threshold, with just £23 separating it from the £12,570 personal allowance.

Should the pension breach this limit following next year's increase, a portion would become subject to the basic 20 per cent tax rate.

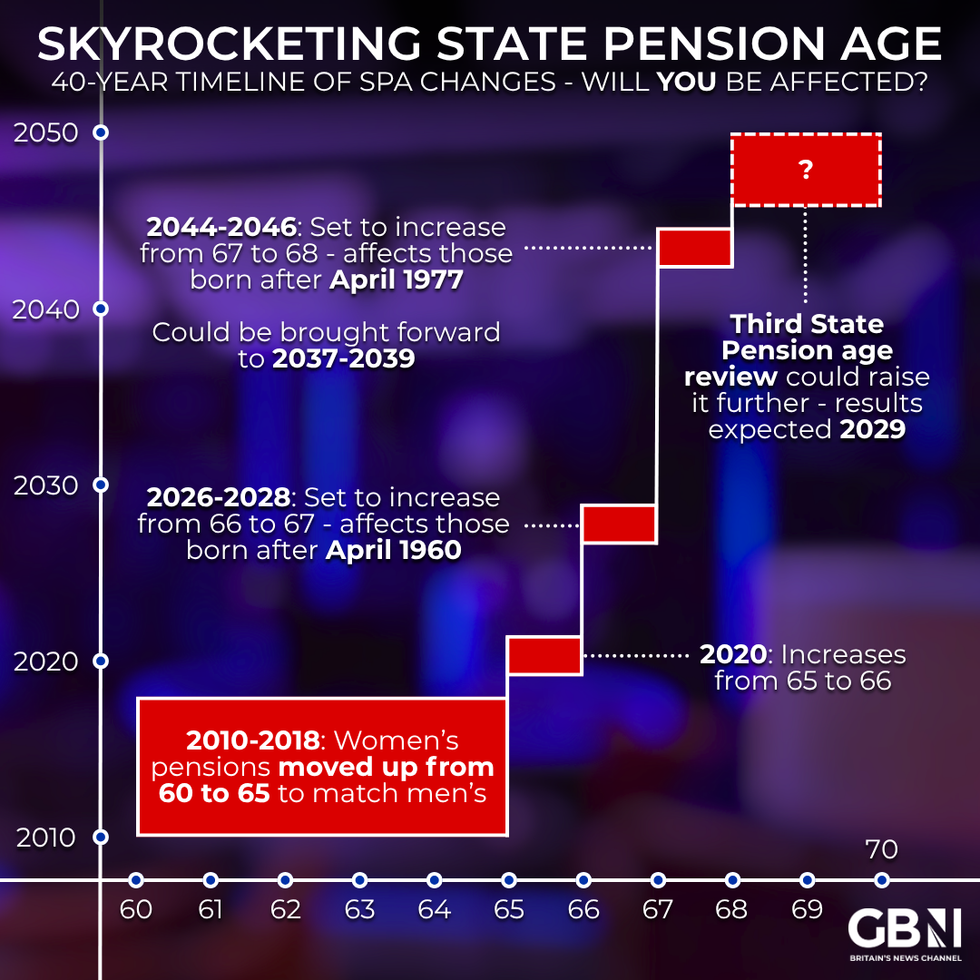

Skyrocketing state pension age - will you be affected? | GB News

Skyrocketing state pension age - will you be affected? | GB NewsMs Smith warned: "For example assuming just the minimum 2.5 per cent increase is applied, the new state pension would rise to £12,861 and £58 of tax would be owed."

While numerous pensioners already face income tax due to private pensions or other earnings, particular concern has focused on vulnerable individuals whose sole income comes from the state pension.

Forecasts suggest inflation may climb in coming months due to ongoing Middle East tensions, potentially affecting future calculations. The Chancellor has stated that pensioners relying exclusively on the state pension will not face income tax during this parliamentary term.

The pension expert highlighted concerns about equity, noting: "This solution also raises questions of fairness, as those with very small private pension income and those working on a wage similar to the state pension would still be expected to pay their tax bill.

"The Government needs to outline their long-term plans for the possible tax liability that looms for millions of state pensioners, enabling them to feel more confident in their financial situation and plans for the future."