A public policy think tank has put forward a radical proposal that would enable workers between the ages of 28 and 40 to withdraw a year's worth of their state pension early.

The Social Market Foundation is calling for eligible individuals to receive £12,548, equivalent to the current full new state pension, as a one-off payment during their working years.

To qualify for this early access, workers would need to have accumulated a minimum of ten years' worth of national insurance contributions.

In exchange for receiving the money decades ahead of schedule, participants would delay their eventual state pension by one year.

A plan to give Gen Z state pension payments early has been slammed

|GETTY

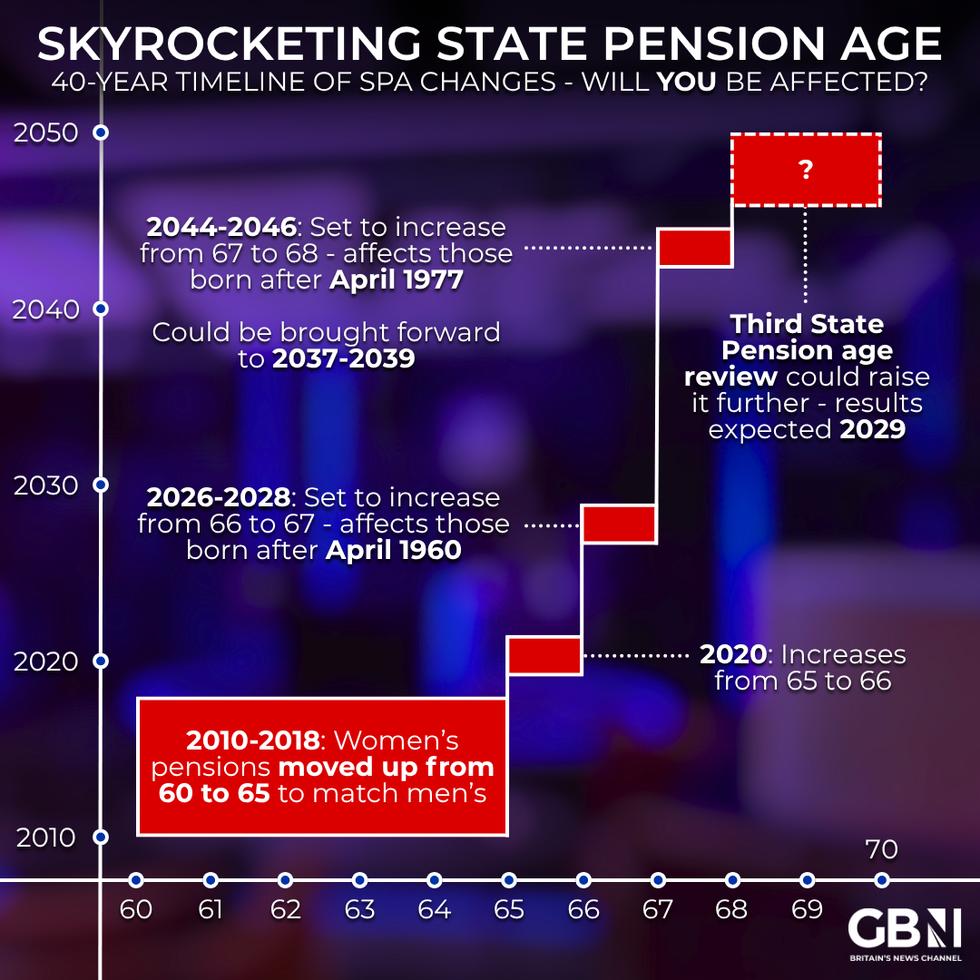

As it stands, the state pension age stands at 66, though this is set to increase to 67 by 2028 and subsequently to 68 between 2044 and 2046.

The think tank argues this scheme would address Britain's growing wealth divide by supporting those who lack affluent families to help them onto the property ladder or eliminate outstanding debts.

Angeline Ong, senior investments analyst at IG, said: "This is another classic buy now, pay later idea, taking from the future to fund the present, and that sends exactly the wrong message when the Government is supposed to be encouraging people to save responsibly for retirement.

"There’s no free lunch here - if you pull one year of state pension forward, you simply shift the pressure somewhere else. With public finances already stretched, that money must come from somewhere.

"Ultimately if this goes ahead, this means less headroom for things like the NHS and welfare, which are already under strain.

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL LATEST DEVELOPMENTS

Are you affected by state pension age changes? | GBN

Are you affected by state pension age changes? | GBN"People are clearly under pressure, especially first-time buyers, and young families, but raiding pension savings early is not a real fix. The more durable answer is to drive growth, back investment, and create better-paying jobs and opportunities because that is what builds confidence and prosperity over time."

Jamie Gollings from the Social Market Foundation said: "Britain is facing a crisis of opportunity. Whether you can buy a home, pay down debt or start a family increasingly depends on the wealth of the parents you were born to, not the work you have put in.

"We urge policymakers to seriously explore this radical and fiscally credible policy proposal. The cost of inaction is a generation locked out of homeownership, drowning in debt, and losing faith that the system can work for them at all."

Research from the Resolution Foundation indicates that roughly one-third of adults anticipate receiving an inheritance or financial gift from relatives during their lifetime.

The foundation estimates the policy would carry a price tag ranging from £1.3billion to £45billion in its inaugural year, with the final figure dependent on which age brackets are included.

The Tony Blair Institute has called for state pension reform

| PAIf restricted to an untaxed £12,500 payment for those born from 1998 onwards with the requisite contribution history, costs would sit at the lower end.

Extending eligibility to workers aged 28 to 35 would push expenditure to approximately £27billion, while including everyone up to 40 would reach the £45billion ceiling.

The think tank noted that taxation or means testing could reduce the burden on public finances. When surveyed, more than half of the 2,000 respondents aged 24 to 40 indicated they would opt for early access, with debt repayment being the most popular intended use.

Tom Selby, the director of pension policy at AJ Bell, acknowledged that the scheme could provide a vital financial boost when people need it most, particularly for those attempting to save for a first-home deposit.

He said: "The obvious potential benefit is that it could deliver a much-needed cash boost at a time many people really need it, particularly if they are trying to save for a deposit on a first home. The downside is that in doing so they would have one year less of state pension income in later life."

Mr Selby cautioned that given widespread uncertainty about the state pension's future, many younger workers would likely seize the opportunity to access funds immediately.