A new report warns that up to 430,000 households across England face the prospect of becoming "climate mortgage prisoners" by 2050 as flooding risks intensify.

The research, titled Flooding the Market: The Climate Mortgage Trap, was produced by Public First on behalf of the UK Sustainable Investment and Finance Association (UKSIF).

According to the findings, homeowners in flood-vulnerable areas risk finding themselves stuck with properties they cannot sell while paying elevated mortgage rates.

The analysis identifies the low-lying constituency of Boston and Skegness as facing the greatest exposure, potentially becoming what the report describes as the "climate mortgage prisoner capital of England".

Analysts warn a property crisis looms as 430,000 Britons could become 'climate mortgage prisoners' due to flooding

|GETTY

Property values in the most flood-prone locations could fall by more than 20 per cent, the research suggests, with consequences extending beyond individual finances to potentially destabilising the broader housing market.

The mechanism trapping homeowners begins when insurers either raise premiums substantially or refuse to renew coverage altogether for properties in flood-prone locations.

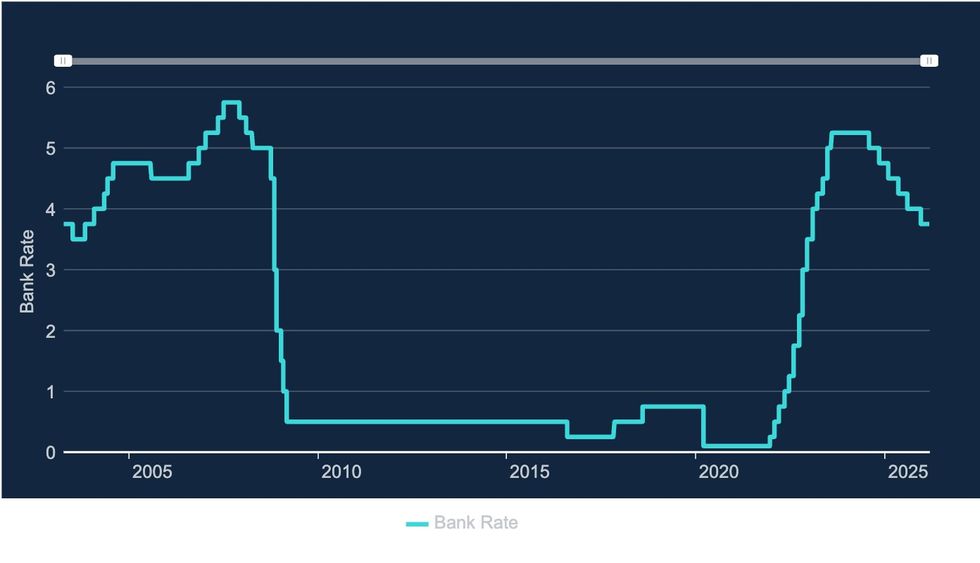

Without affordable insurance, mortgage holders reaching the end of fixed-rate deals may find themselves forced onto standard variable rates, which currently sit at approximately seven per cent.

This shift could mean paying around £4,000 more in annual interest payments – a sum nearly equivalent to what a typical UK household spends yearly on food and non-alcoholic drinks.

Bank of England interest rates over time | Bank of England

Bank of England interest rates over time | Bank of England LATEST DEVELOPMENTS

Britain has been impacted by flooding issues

| PAUninsured households also face potential repair bills reaching £45,000 to restore their homes following storm damage. These properties become extremely difficult to sell since buyers cannot secure mortgages or remortgages on them, while cash purchasers show little appetite for such risky investments.

The report's authors caution that growing numbers of homeowners unable to obtain fixed-rate mortgages would represent an "unprecedented scenario" for the market.

Concentrations of mortgage prisoners within communities could restrict lending flows and spark localised credit crunches, placing strain on financial services.

Such conditions may extend selling times and depress prices, potentially triggering collateral write-downs on lenders' balance sheets that could unsettle the housing market more broadly.

Interest rates could stay high if prices are increased for long enough to affect the rate of inflation | GETTY

Interest rates could stay high if prices are increased for long enough to affect the rate of inflation | GETTY Banks may begin limiting lending in vulnerable areas well before that deadline, the report warns, "potentially by the end of this parliament". The geographic impact of climate change on housing will be heavily concentrated in specific regions, the research reveals.

Beyond Boston and Skegness with its 8,600 at-risk mortgaged homes, Thurrock follows with 7,700 properties exposed, then Goole and Pocklington at 6,900.

South Basildon and East Thurrock, Bootle, Sefton Central, Louth and Horncastle, Southport, Hastings and Rye, and Rayleigh and Wickford complete the ten most vulnerable constituencies.

Some neighbourhoods could become "impoverished and/or abandoned" entirely, according to the analysis. The price drops exceeding 20 per cent in high-risk zones could push borrowers into negative equity.

Meanwhile, demand shifting towards safer locations could drive prices up by as much as eight per cent in low-risk areas, making homeownership increasingly "unattainable for many young people and families looking to get on the housing ladder".

The report calls for mandatory Flood Performance Certificates for properties, similar to existing Energy Performance Certificates (EPC), alongside confirmation of FloodRe's future before parliament ends to prevent a "cliff-edge" scenario.

Amy Norman, Director at Public First, said: "For most British families, their home is their single biggest source of wealth. But weather risks like the flooding we saw this winter are starting to erode that, as some properties become harder to insure and mortgage."

James Alexander, UKSIF's chief executive, described the findings as "a warning about the urgent need to prioritise climate adaptation and resilience strategies that protect both households and the financial sector."

Aviva's UK general insurance chief Jason Storah added that insurers are "sending a clear signal to Government that planning and building regulations need to be strengthened".