Rising living costs are pushing growing numbers of British pensioners back into employment, as inflation continues to erode the value of fixed retirement incomes.

Research from Standard Life indicates that one in six retirees has either already re-entered the workforce or is actively considering doing so in response to mounting financial pressure.

The scale of the challenge is underlined by analysis showing that £100 held in 2020 now carries the purchasing power of just £78.25, reflecting the sustained impact of inflation on household finances.

A longer-term trend of older workers supplementing their income had briefly reversed during the pandemic, when some individuals opted for early retirement, but has since resumed an upward trajectory.

TRENDING

Stories

Videos

Your Say

Data analysed by the pension provider shows the proportion of pensioners earning wages increased from 6 per cent to 7 per cent between 2022-23 and 2023-24.

For some, the return to work has been driven by necessity rather than choice, with financial resilience in retirement proving increasingly difficult to maintain.

Trevor Chambers, 66, was compelled to re-enter employment at the age of 62 after concluding that his savings alone would not be sufficient to cover ongoing expenses.

After a career at Southampton Port involving demanding shifts that often began at 4am and lasted up to 12 hours, he took on two part-time roles, invigilating exams at a local school and working in a warehouse twice a week, travelling by bicycle to reduce fuel costs.

UK pensioners return to work as inflation cuts retirement income

|GETTY

Mr Chambers told the Telegraph that the experience “absolutely destroyed” him.

“I resented being there. I struggled massively,” he added, describing the return to work as a profound psychological shock despite decades of employment behind him.

“It was like going back to school,” he said.

A major factor in his decision was fear of running down his savings.

“There are so many unforeseen expenses in your later years that you feel really vulnerable with nothing in the bank,” he said.

LATEST DEVELOPMENTS:

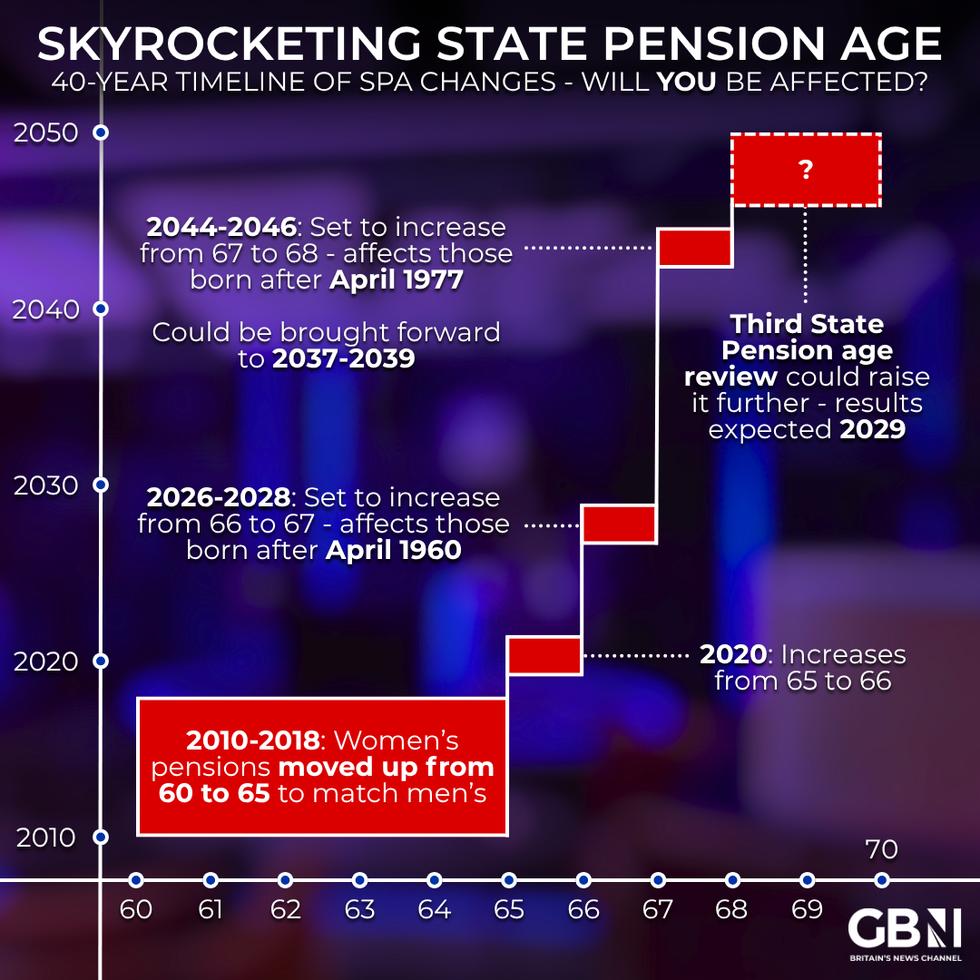

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYWider economic conditions continue to add pressure, with food prices rising at an annual rate of 3.5 per cent, according to the British Retail Consortium, and staple items such as meat and coffee among the fastest increases.

Policy decisions have also been cited as contributing factors, particularly changes to support measures affecting pensioners.

Dennis Reed, representing the charity Silver Voices, pointed to the temporary suspension of winter fuel payments in 2024 as having a notable impact.

Mr Reed said: “The decision was particularly damaging when accentuated by the sharp rise in utility and council tax bills and food prices from April 2025, which far outweighed the triple lock increase.”

He added that sustained cost pressures are limiting the ability of individuals to maintain or build private pension savings.

Mr Reed said: “It is hardly surprising that increasing numbers of pensioners are being forced back to work to make ends meet.”

While financial necessity is a driving factor for many, some retirees continue to view part-time work as a planned component of their retirement strategy.

Iain Thomas Morgan, 67, from Cornwall, had anticipated supplementing his income after leaving full-time employment following 25 years in the food industry.

His current routine includes delivering parcels four days a week alongside undertaking school transport work through an agency, allowing him to maintain a steady income stream.

Mr Morgan said: “My workplace pension wasn't a substantial amount, so I knew it wouldn't go very far on drawdown.”

Maintaining a desired lifestyle remains a priority, with regular travel forming part of his plans while his private pension remains untouched.

He said: “I'd rather keep that for later and carry on working in a way that suits me.”

The arrangement enables continued income generation while supporting a more flexible approach to retirement, reflecting the varied experiences of pensioners navigating current economic conditions.