Chancellor Rachel Reeves is understood to be planning to abolish a pension bonus linked to lifetime ISAs as part of its reforms to the saving product.

The Labour Government is set to axe the lifetime Isa in favour of a new savings vehicle aimed solely at those purchasing their first property, with the replacement set to launch in April 2028.

Notably, the Government's revamped product will remove the option to save towards retirement entirely, focusing exclusively on helping people onto the housing ladder.

Under the proposed changes, the 25 per cent Government top-up will no longer be credited monthly but instead paid as a lump sum when a first home is purchased.

The Chancellor is preparing drastic overhaul to the ISA regime

|GETTYH

This shift means account holders will forfeit the opportunity to earn interest or investment returns on the bonus throughout their saving period.

The existing lifetime Isa permits savers to contribute up to £4,000 annually, with the Government adding a tax-free 25 per cent bonus that brings the maximum yearly total to £5,000.

Current rules allow withdrawals either for purchasing a first home valued at no more than £450,000 or for retirement once the holder reaches 60.

Those who access their funds for any other purpose face a penalty that claws back not only the government bonus but also 6.25 per cent of their own contributions.

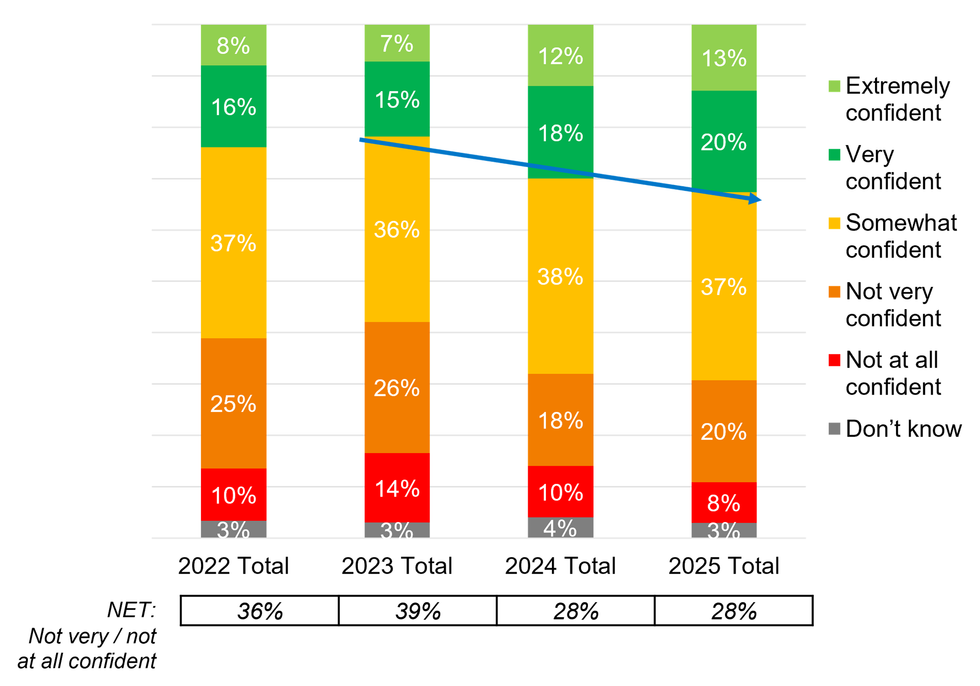

How confident are Britons about their pension savings? | AEGON

How confident are Britons about their pension savings? | AEGON The Treasury has confirmed the replacement product will eliminate withdrawal penalties, though whether the property price ceiling will be adjusted remains unclear.

Financial experts have voiced concerns about the proposed changes, warning that savers stand to lose significantly.

David Horowitz, the head of financial planning at Gerald Edelman, said: "If investment growth ultimately isn't allowed, the majority of people will be disincentivised to use this as a product. The whole point of an Isa is tax-sheltered investment growth."

Rachael Griffin, tax and financial planning wealth manager Quilter, cautioned that account holders could sacrifice years of potential returns on their savings.

She said: "Trying to make one product serve both first-time buyers and retirement savers has never really worked in practice. The Lifetime Isa's dual purpose has long added unnecessary complexity and uncertainty for savers."

A Treasury spokesman said: "We recognise that the Lifetime Isa is not working for everyone, particularly when people's circumstances change.

"That is why we intend to consult on a new and improved product, specifically designed to support first-time buyers and without penalty for withdrawals."

The consultation follows Ms Reeves's November Budget pledge to deliver a "simpler" savings product, after a Treasury Select Committee review branded the existing penalty a "perverse incentive" that punished savers.

ISAs are popular savings tools | GETTY

ISAs are popular savings tools | GETTYAs part of broader Isa reforms, the Chancellor has also reduced the annual cash Isa allowance for those under 65 from £20,000 to £12,000, effective from April 2027.

Recent analysis of CACI data between January and October 2025 revealed that savers transitioned towards tax-efficient savings ahead of the reduction in the cash ISA allowance.

Over the time, the average adult cash ISA balance increased from £15,919 to £17,019, while the average non-ISA balance fell from £11,918 to £11,710.

Total adult cash ISA balances rose by £51.4billion during the period, with much of the growth driven by strong demand for fixed-term products. Overall, adult cash ISA balances in accounts totalled £430.1billion across 25 million accounts at October 2025.

More From GB News