Pension pots are set to become liable for inheritance tax (IHT) next year as part of reforms previously announced by Chancellor Rachel Reeves, with analysts urging Britons to "rethink assets" ahead of the raid.

The forthcoming inclusion of pensions within inheritance tax calculations from 2027 is driving investors to reassess how they structure and transfer their wealth.

This regulatory shift has placed renewed emphasis on portfolio income, particularly where it enables regular tax-efficient gifts without depleting underlying capital.

Current market conditions are bolstering the appeal of fixed-income investments. Following several years of rising interest rates, bond markets now present yields that have been absent for more than ten years.

Pension pots are set to be slapped with inheritance tax from next year

|GETTY

Risks are also more transparently priced, creating what experts describe as a notably different landscape for bond investors compared to recent history.

Bryn Jones, head of fixed income at Rathbones, said: "After several years of rising interest rates, bond markets are offering income levels not seen for over a decade, while risks are more clearly priced.

"It is a very different backdrop for bonds than investors have seen for a long time, offering relatively rare opportunities. It's not often you get a chance to invest in positive real income available across of the credit spectrum."

Mr Jones also POINTED to enhanced risk-return profiles supporting fixed income assets.

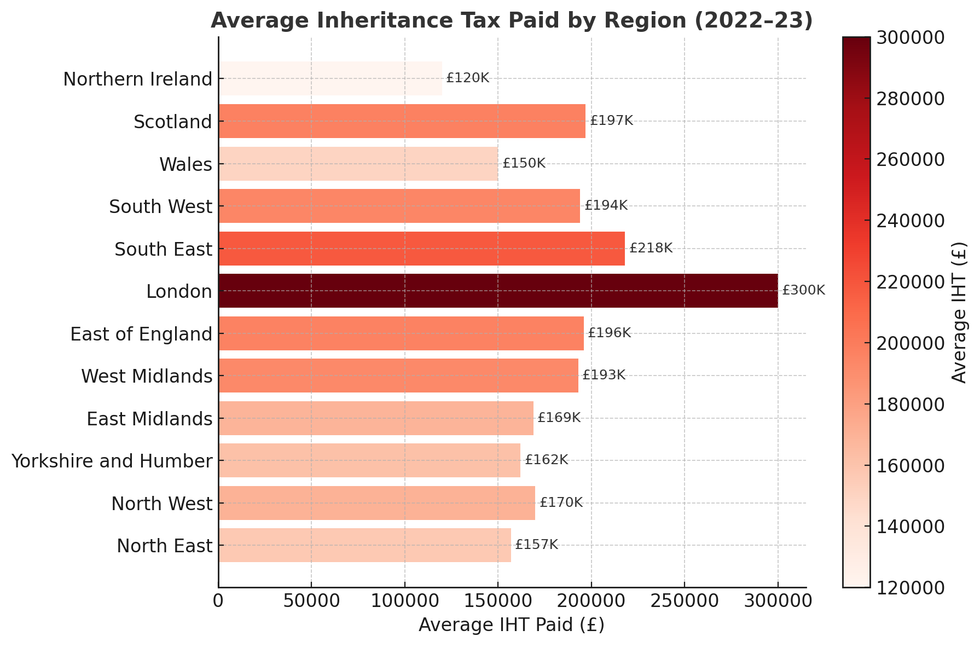

Average Inheritance tax paid by region | CHATGPT/ONS

Average Inheritance tax paid by region | CHATGPT/ONSLATEST DEVELOPMENTS

How much pension tax relief you can get depends on your earnings | AJ Bell analysis of HMRC data

How much pension tax relief you can get depends on your earnings | AJ Bell analysis of HMRC dataThe tax specialist noted that elevated starting yields combined with shorter duration across bond indices are making risk-adjusted returns more compelling.

Bonds additionally serve a crucial function in portfolio diversification and volatility management, particularly during periods of geopolitical tension or equity market weakness.

Richard Cook, senior financial planner at Rathbones, comments: "The inclusion of pensions within IHT from 2027 is prompting a broader rethink around how assets are used over time.

"It is clear that one area that is coming into sharper focus is the distinction between capital and income, particularly in the context of passing on wealth."

The Chancellor's inheritance tax changes are under fire

| POOLMr Cook explained that when income surpasses everyday living costs, it generates flexibility for investors: "The ability to generate a consistent income stream without eroding capital is increasingly relevant in the current environment."

For investors focused on income generation, particularly those utilising ISAs and SIPPs, the elevated yields significantly enhance the contribution bonds can make to their portfolios.

"Sheltering income within ISAs and SIPPs, and allowing it to compound, can be powerful over the long term," Mr Cook added.

"As the 2027 changes approach, income is becoming a more prominent part of the overall conversation, not just for portfolio construction, but in how wealth may ultimately be used."