Homeowners across Britain are confronting substantially higher borrowing costs following the outbreak of conflict in Iran, according to mortgage app provider Sprive.

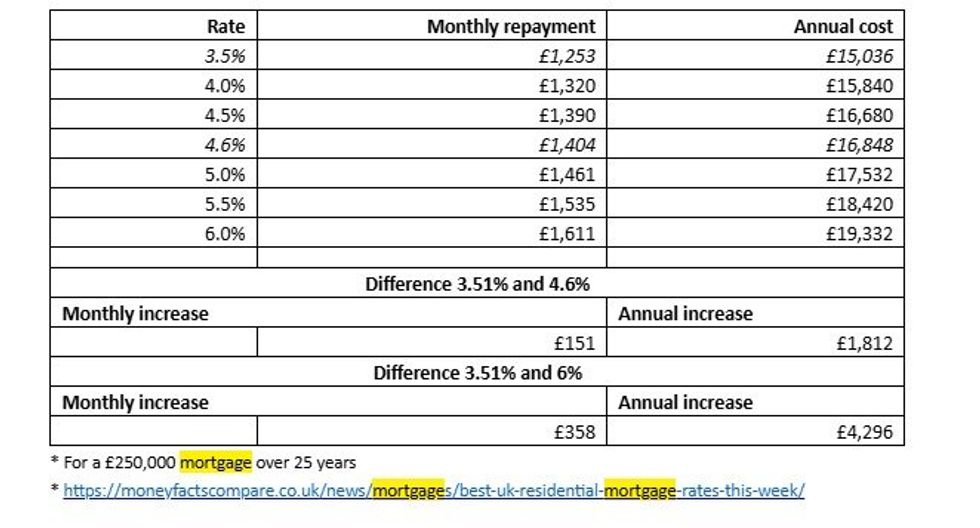

Data from Moneyfacts reveals that the cheapest two-year fixed mortgage available before hostilities commenced stood at 3.51 per cent, but this has since surged to 4.6 per cent.

This shift translates to an additional £151 monthly, or £1,812 over a year, however, analysts note that these figures represent only the most competitive deals on the market.

Typical rates have now climbed to approximately five per cent, with numerous lenders pushing their offerings beyond six per cent this week, potentially leaving borrowers facing annual increases of up to £4,300.

Mortgages are expected to jump by £4,300 in response to the Middle East conflict

|GETTY

Jinesh Vohra, the chief executive of Sprive, highlighted the speed at which international developments, such as the US-Iran war, can affect domestic lending markets.

He said: "The jump in rates in just a few weeks shows how quickly global events can ripple through the mortgage market and expose homeowners to higher costs.

"With rates going past five per cent last week and now many creeping over six per cent, the impact is immediate for those looking to buy, remortgage, or sell."

The mortgage expert warned that market volatility often prompts lenders to withdraw products or impose stricter lending requirements, dramatically reducing the options available to borrowers within days.

What will you need to pay in terms of mortgage costs?

|MONEYFACTS /SPRIVE

LATEST DEVELOPMENTS

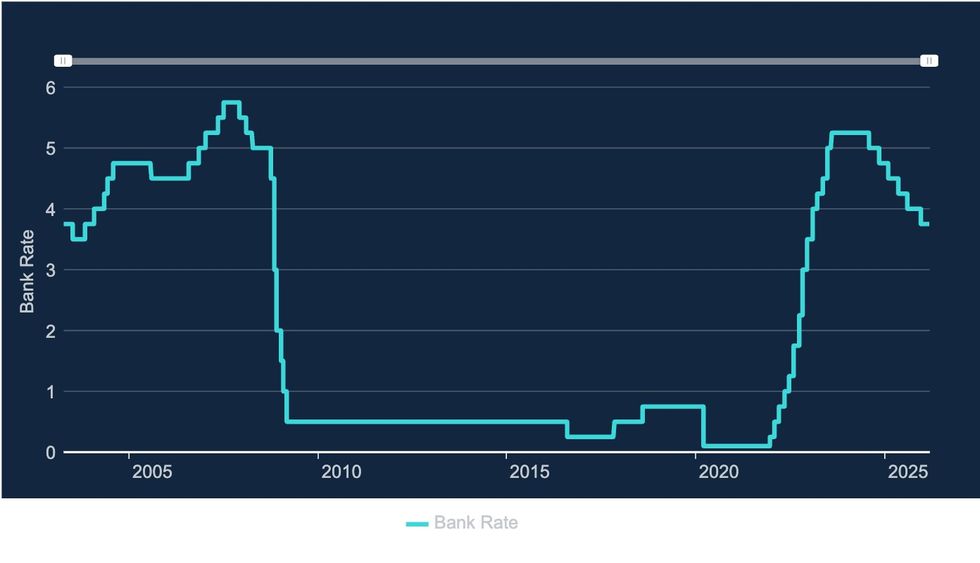

Bank of England interest rates over time | Bank of England

Bank of England interest rates over time | Bank of England Mr Vohra urged property owners to take a proactive stance rather than waiting for conditions to improve.

He said: "Homeowners need to act proactively: review their deals early, lock in fixed rates where possible, and overpay if they can to reduce interest costs."

The Sprive chief executive noted that digital tools can assist borrowers by tracking daily market movements, identifying optimal remortgage timing, and enabling gradual mortgage reduction.

This could be through cashback from routine purchases and helping households build financial resilience without significant lifestyle adjustments.

Millions of households face 'mortgage shock' | GETTY

Millions of households face 'mortgage shock' | GETTY Adam French, the head of Consumer Finance at Moneyfacts, said: "The conflict in Iran quickly upended rate expectations and sent borrowing costs skyrocketing in the biggest shock to the UK mortgage market since the aftermath of the 2022 mini-Budget.

"For many borrowers, the cost could be significant. Someone taking out a typical two-year fix will find it costs £150 more per month on average compared to just a few weeks ago.

"However, the real payment shock will be felt by those coming off older five-year deals, where rates have more than doubled, pushing up repayments by many hundreds of pounds per month.

"The combination of rising rates, reduced choice, and heightened volatility means borrowers and brokers are operating in a market where timing is critical, and the window to secure competitive deals can be very short-lived. Unfortunately, anyone looking to buy or remortgage this year needs to prepare for substantially higher borrowing costs than expected before this conflict began."