British savers face a tighter window than usual to maximise their £20,000 tax-free ISA allowance this year, with financial experts warning that April 3 is effectively the final day to act.

Although the tax year officially concludes on April 5, the Easter bank holiday weekend means anyone wishing to make changes must do so before the long weekend begins.

Rachael Griffin, tax and financial planning expert at Quilter, said: "With the tax year ending on Sunday, anyone needing to make changes will, in practice, need to act by April 3. Time is tighter than usual this year, given the bank holiday weekend, so it is sensible to check now that you are using your allowances before they reset."

It should be noted that any portion of the annual tax-free allowance attached to ISA products left unused cannot be carried forward and is permanently forfeited.

The ISA deadline is only days away

|GETTY

Despite recent market turbulence making some investors hesitant, financial advisers are encouraging savers to press ahead with their contributions.

Alec Collie, financial planning expert at Wesleyan Financial Services, said: "The end of the tax year is a crucial moment for savers. Once the deadline passes, any unused ISA allowance is lost forever."

He added: "Periods of market volatility, like we've seen recently, can understandably make investors nervous about topping up their ISA. But staying invested and continuing to contribute regularly is often key to the best results over the long term. The old adage still applies – it's about time in the market, not timing the market."

For those uncomfortable with sharp fluctuations in their portfolio value, much of which results from the US-Iran war, Mr Collie suggested smoothed funds as an alternative.

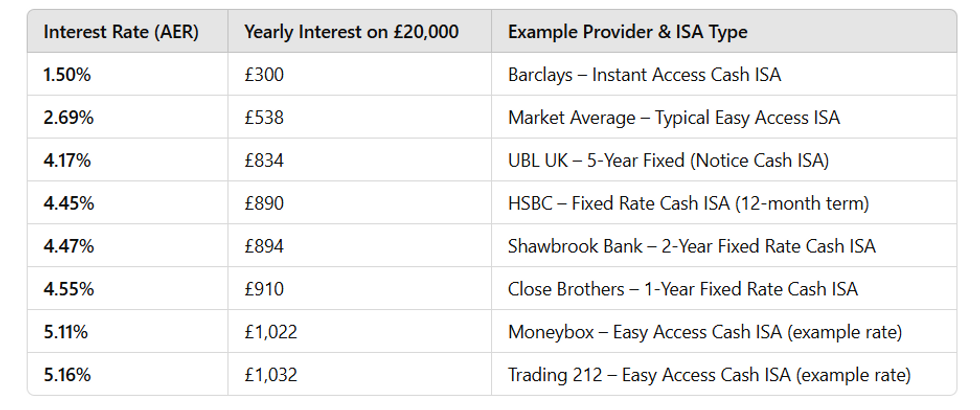

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBN

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBNLATEST DEVELOPMENTS

- Premium Bonds alert: Long wait for NS&I prizes as YOU could 'be better off putting cash elsewhere'

- 'I don't spend a penny on energy bills!' Pensioner explains how he cut his bill to £0 in retirement

- Second NS&I boss quits amid £476million missing savings scandal

ISAs are popular savings products are becoming increasingly popular | GETTY

ISAs are popular savings products are becoming increasingly popular | GETTYThese investment vehicles function similarly to shock absorbers, holding back some gains to cushion against downturns and deliver a steadier experience during choppy conditions.

However, research suggests many savers are failing to actively manage their ISA investments. A survey of 1,000 UK Stocks and Shares ISA holders revealed a widespread "set and forget" mentality that could prove costly over time.

The findings showed that 14 per cent of respondents largely leave their ISA to run without intervention, while one in twenty never conduct regular reviews at all. Fee awareness also appears worryingly low, with more than half of holders unaware of what charges they pay.

Meanwhile, two-thirds have never switched provider, with nearly four in ten citing an assumption that their existing arrangement was adequate. Most holders are also unaware they can spread their allowance across multiple providers in the same tax year, provided they remain within the £20,000 limit.

The ISA allowance resets each year on April 6, when a new tax year begins | GETTY

The ISA allowance resets each year on April 6, when a new tax year begins | GETTYLooking beyond this week's deadline, savers should also prepare for significant changes to the tax landscape arriving in 2027.

Ms Griffin warned: "This is a year to use the allowances you can, but the bigger task is getting ready for the major structural shifts arriving in 2027.

"Cash ISA limits will be cut for under-65s and savings income will be taxed more heavily, while unused pensions will fall within IHT, so households need to think beyond this week's deadline and prepare for a very different tax landscape."

These reforms will fundamentally alter how households approach tax-efficient saving, with younger savers facing reduced shelter for their cash holdings and pension pots becoming subject to inheritance tax for the first time.