State pension age increases risk contributing to a "growing crisis" as millions of older Britons "struggle to make ends meet", analysts have warned.

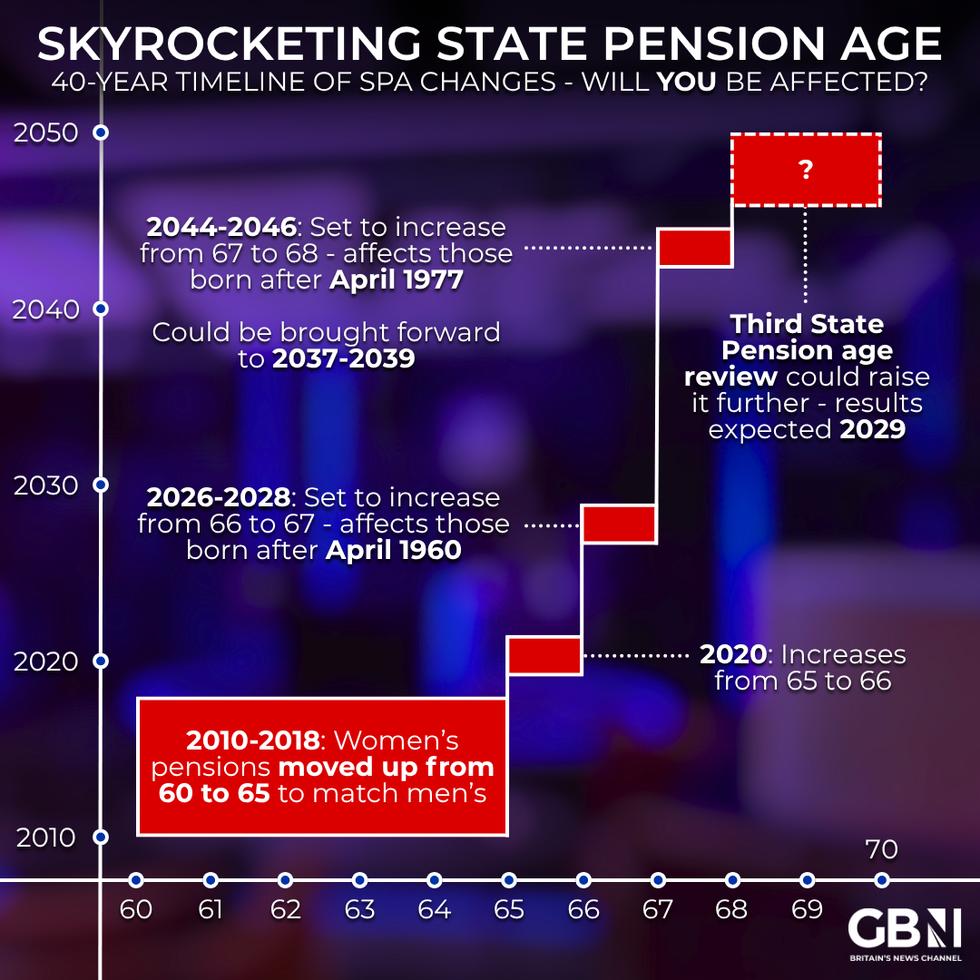

With the state pension age set to rise from 66 to 67 beginning from this month, research reveals the stark financial pressures facing older workers waiting to claim their entitlement.

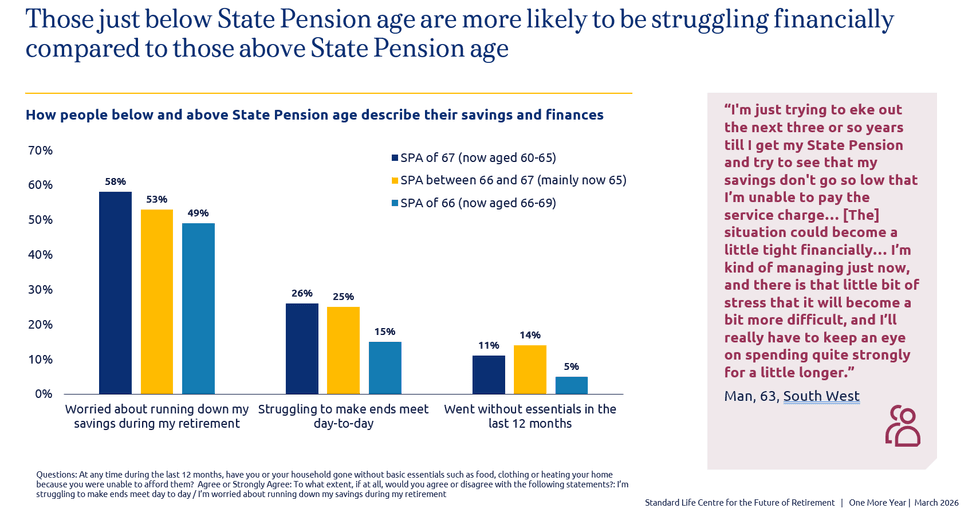

Findings from the Standard Life Centre for the Future of Retirement show that individuals currently just under state pension age are nearly three times as likely to have foregone basic necessities such as food, clothing or heating over the past year.

The study found 14 per cent of those approaching pension age had gone without essentials, compared with just five per cent of people aged 66 to 69 who already receive their state pension.

Experts have issued a warning over a growing state pension age 'crisis'

|GETTY

The research examined the transition group that will be first affected by the forthcoming increase in the qualifying age.

A quarter of people in their early 60s reported struggling to cover everyday expenses, a figure that drops to one in seven among those already receiving their state pension.

Separate analysis from the same research centre found that 250,000 additional people aged 60 to 64 now live in relative income poverty compared with 2010, a rise attributed largely to successive increases in the retirement age.

The burden falls disproportionately on lower earners, with a fifth of those earning under £25,000 saying the pension age rise will significantly affect their household finances, compared with just one in ten earning £50,000 or more.

How do Britons above and below the state pension age refer to their savings and finances? | STANDARD LIEF

How do Britons above and below the state pension age refer to their savings and finances? | STANDARD LIEF LATEST DEVELOPMENTS

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYFor the poorest fifth of households containing someone aged 66 to 70 where nobody works, the state pension accounts for nearly three-quarters of total income.

This dependency creates particular vulnerability, with a majority of Generation X, the oldest of whom have now entered their 60s, projected to rely heavily or entirely on the state pension in retirement.

To bridge the gap until they qualify, more than a third of non-retired people in their early 60s say they will need to extend their working lives. Around a quarter plan to dip into personal savings or private pensions, while eight per cent intend to claim Universal Credit or other benefits.

Those aged 60 to 65 are also more likely than pension recipients to cite needing money for daily expenses as their reason for continuing to work.

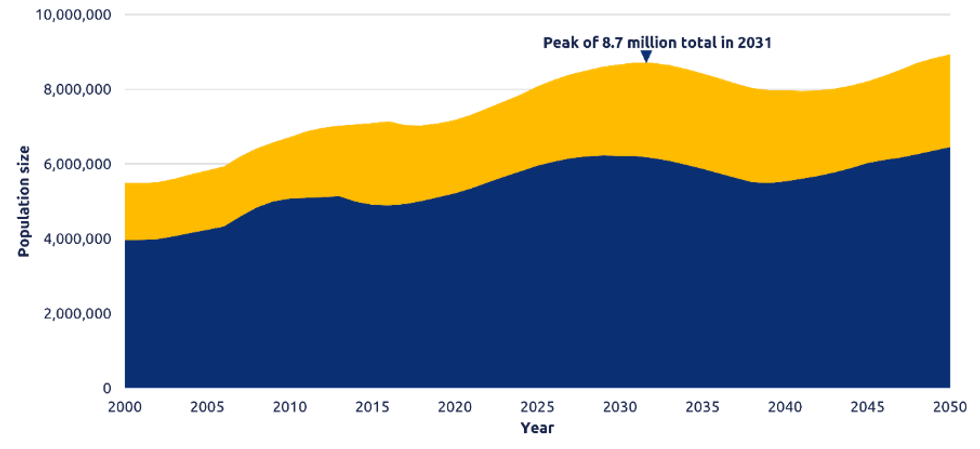

Projection of the total number of people aged 60-66 and 67-69: UK, 2000 to 2050 | STANDARD LIFE

Projection of the total number of people aged 60-66 and 67-69: UK, 2000 to 2050 | STANDARD LIFE Patrick Thomson, the head of Research Analysis and Policy at the Standard Life Centre for the Future of Retirement, said: "We face a growing crisis in which too many people in their 60s are struggling to make ends meet as the state pension age rises.

"Without action, this will worsen the widespread pension under-saving problem, and the government must set out a clear plan to improve financial security so the most vulnerable are supported before and during retirement."

He noted that women are significantly more affected than men, as are those on lower incomes who depend more heavily on the state pension.

The increase from 66 to 67 is expected to save the government approximately £10billion annually, though Mr Thomson warned much of this will simply be diverted from people's personal retirement savings or redirected into other benefit claims.