State pension age increases over the years have come at "significant human cost", analyst are warning amid calls to raise the threshold at which someone accesses retirement payments to 70.

Fresh analysis from the Standard Life Centre for the Future of Retirement exposes the mounting financial crisis among Britain's pre-retirement population, with poverty rates soaring to unprecedented levels.

The Government is in the process of carrying out a State Pension Age review as concerns grow over the long-term viability of the triple lock, which is the mechanism used to determine annual payment hikes.

Currently, 25 per cent of individuals between 60 and 65 years old experience poverty conditions - representing 800,000 additional people compared with 2010 figures.

Britons are concerned about the rise in the state pension age | GETTY

Britons are concerned about the rise in the state pension age | GETTYThis demographic faces particularly harsh circumstances, with typical earnings falling 16 per cent below those of people in their late fifties. As part of the latest review, ministers will ministers consider accelerating pension age increases, potentially affecting approximately three million citizens.

Helen Morrisey, the head of personal finances at Hargreaves Lansdown, previously warned: "First and foremost, increasing numbers of pensioners claiming state pensions for longer time periods are pushing up the state pension bill.

"It’s an issue front and centre of Government with a review into state pension age ongoing. Potential options to mitigate the bill could include reform of the triple lock mechanism used to increase the state pension every year.

"We will also likely see further discussion on whether the timetable for state pension age rises needs to accelerate even further and we could see a timetable put in place for a state pension age rising into the 70s."

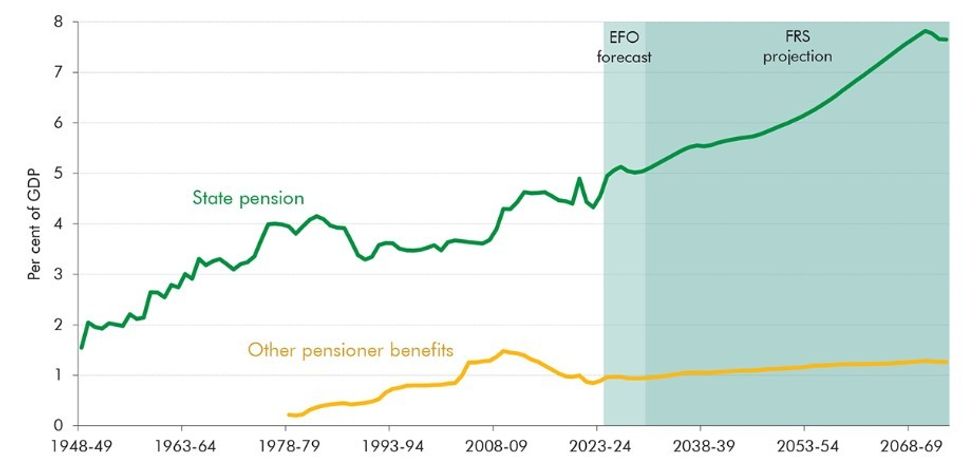

How much will the state pension triple lock cost the British taxpayer? | OBR

How much will the state pension triple lock cost the British taxpayer? | OBR The data reveals a troubling employment landscape for those approaching retirement, with two-fifths of early-sixties individuals already absent from the workforce.

Among Britain's 60-64 age group, approximately 1.7 million people remain economically inactive. Health challenges constitute the primary barrier, with 37 per cent of this inactive population citing chronic illness or disability as their principal reason for leaving employment.

These figures underscore the impossibility of extending working lives for substantial numbers who face physical limitations.

Financial precarity extends beyond employment status, with 40 per cent of those between 60 and 65 possessing under £3,000 in personal savings.

Research indicates that 35 per cent of unemployed individuals in poverty within this age bracket belong to households receiving private pensions but no government support.

Those aged 50-64 who elect to retire possess median assets exceeding £1.2million, while individuals forced from employment through chronic health conditions hold median wealth of merely £57,000, less than five per cent of their healthier counterparts' resources.

LATEST DEVELOPMENTS:

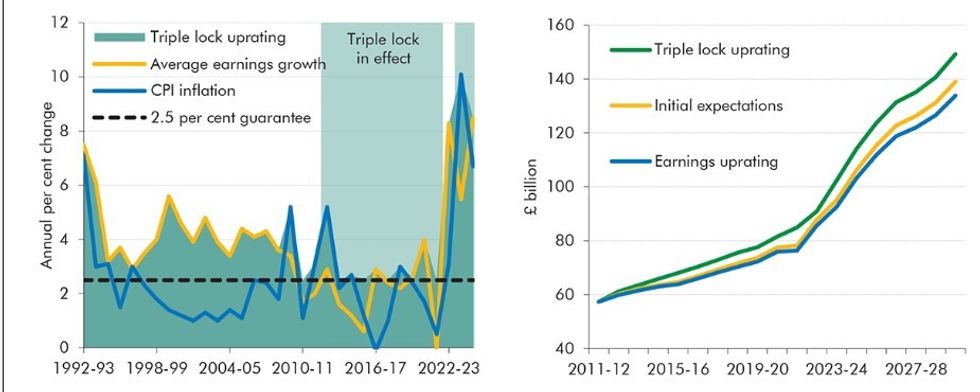

What has the impact of the state pension triple lock been on the public's finances | OBR

What has the impact of the state pension triple lock been on the public's finances | OBR Catherine Foot, who leads the Standard Life Centre for the Future of Retirement, emphasised the human consequences of potential policy changes.

"Affordability will always be part of the debate about the State Pension Age, especially as our population continues to age. But the evidence shows that previous increases have already come at a significant human cost," she stated.

Ms Foot highlighted the stark reality facing this demographic: "A quarter of people in their early sixties now live in poverty, and many more are unable to work due to poor health or caring responsibilities."

She cautioned that whilst pension age increases might provide temporary fiscal relief, they "risk deepening inequality and hardship for those least able to work for longer."