Finance experts are warning 20 million British savers to avoid these three major mistakes before the upcoming ISA tax-free allowance deadline next month.

Tomos Russell, a portfolio manager at Wealthify, has highlighted three errors he regularly encounters among British ISA holders.

This latest warning comes as figures indicate that more than 20 million people across the UK possess at least one ISA account.

Despite this widespread uptake, Mr Russell questions whether savers are truly getting the best value from these tax-efficient products.

The ISA deadline is only weeks away

|GETTY

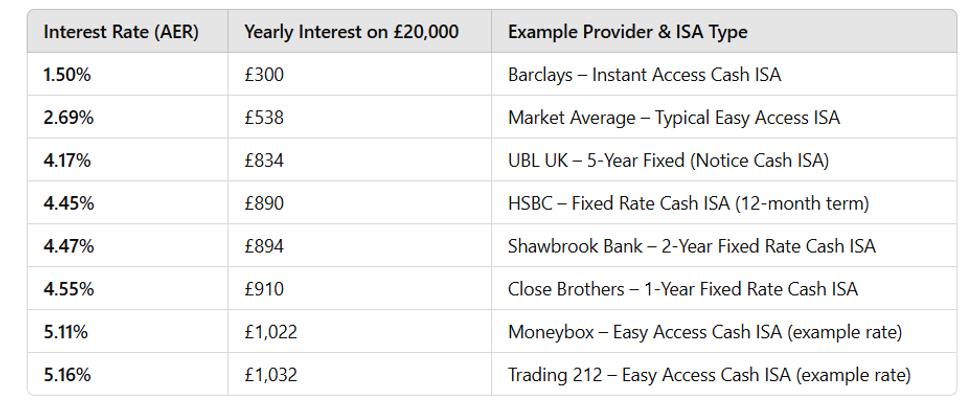

As it stands, savers are able to deposit up to £20,000 into cash ISA accounts without having to pay tax to HM Revenue and Customs (HMRC).

Last year, Chancellor Rachel Reeves confirmed this allowance would be slashed to £12,000 to encourage Britons to invest in stocks and shares ISAs.

The first common mistake Mr Russell identifies is leaving ISA contributions until the final moments of the tax year.

He explained: "Utilising your ISA allowance early in the new tax year can help maximise your returns, as investing gives your money the opportunity to grow over the long term, although returns can rise and fall with market conditions."

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBN

Examples of tax free Isa earnings in the UK if you had £20,000 in the Isa | GBNLATEST DEVELOPMENTS

The change to the cash ISA limit was announced in the 2025 Budget | GETTY

The change to the cash ISA limit was announced in the 2025 Budget | GETTYMr Russell emphasises the power of compounding, describing it as a snowball effect where investors earn returns on both their original sum and any gains already accumulated.

This process can potentially generate exponential growth over time, he notes, meaning those who invest earlier in the tax year may see superior results compared to last-minute savers.

The second error involves overlooking stocks and shares ISAs in favour of traditional cash savings accounts. Mr Russell points out that while cash deposits generate interest, investment options may deliver stronger performance over extended periods.

He said: "While investing carries risk and returns aren't guaranteed, options like Stocks & Shares ISAs can often help you beat inflation over the long term."

Rachel Reeves is preparing significant reform to ISA reform | GETTY

Rachel Reeves is preparing significant reform to ISA reform | GETTY With the Bank of England having reduced interest rates by 0.25 percentage points to 3.75 per cent, and inflation currently standing at three per cent, conventional savings accounts are providing limited growth opportunities.

Mr Russell offers a simple principle for those weighing their options: "Save for what's around the corner but invest for the future." The third mistake Russell highlights is failing to utilise the full £20,000 annual ISA allowance available to each individual.

However, he stresses that consistent contributions over multiple years, even at more modest levels, can significantly boost long-term returns.

For those able to put money aside regularly, the cumulative effect of maximising ISA deposits year after year could prove substantial when it comes to building wealth.

More From GB News