Nearly half a million pension savers emptied their retirement funds entirely upon first accessing them during the 2024-25 financial year.

Data shows that 462,160 pension pots were withdrawn in full during the year, representing a 29 per cent increase compared with the 357,122 recorded during 2018-19.

The figures, released by the Financial Conduct Authority (FCA), have intensified concerns among pension industry experts about the scale of retirement under-saving across Britain, particularly among workers relying on smaller pension pots.

Analysis by wealth management firm Quilter found that around 301,991 of the pension pots fully withdrawn during 2024-25 were valued at less than £10,000.

The average pension pot size has also declined slightly over the past six years, falling from £18,367 during 2018-19 to £17,355 during 2024-25, according to the analysis.

Quilter said smaller pension pots were significantly more likely to be withdrawn in full than larger retirement savings.

Industry experts warned that many savers appear to be accessing their pensions out of financial necessity rather than as part of a planned retirement income strategy.

Adam Cole, policy strategy and affairs director at Quilter, said: "Where savings are limited, taking the full amount is often a practical response to immediate financial pressures rather than a long-term income strategy.

FCA pension warning as 462,000 savers emptied retirement funds completely in 2024-25

|GETTY

"The concern is that fully cashing out smaller pots may provide short-term relief but raises the risk of running out of money later in life."

Georgie Edwards of workplace pension provider TPT described the figures as "a worrying signal" about retirement preparedness in the UK.

She said: "For many, it's not a strategic choice but a sign their savings aren't sufficient."

TPT said the trend suggested growing numbers of workers were approaching retirement without adequate savings to sustain their standard of living in later life.

LATEST DEVELOPMENTS

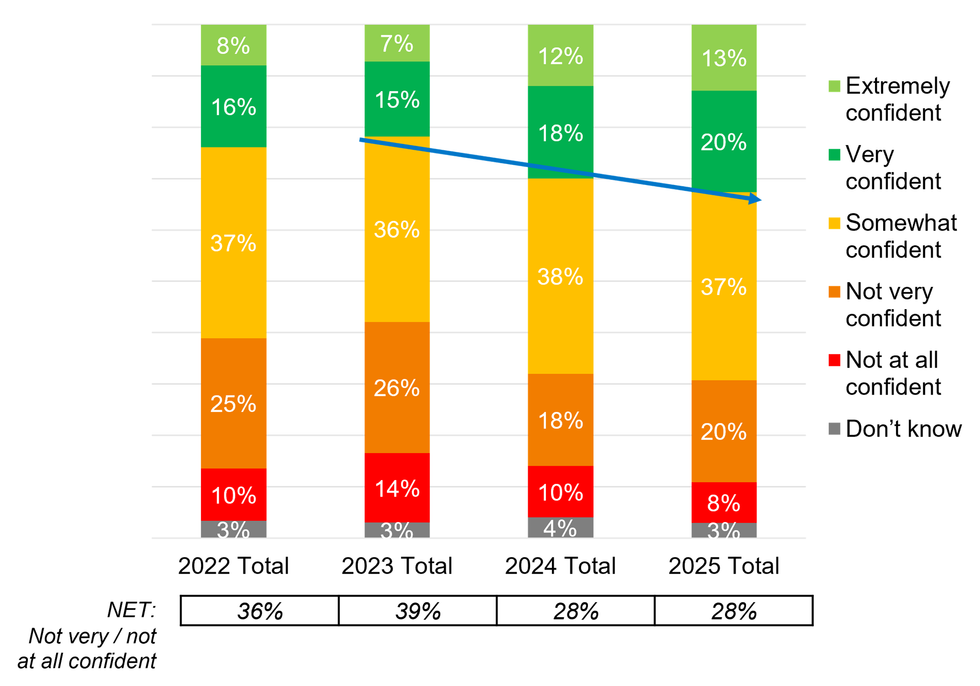

How confident are Britons about their pension savings? | AEGON

How confident are Britons about their pension savings? | AEGON The warnings come as Labour has ruled out increasing mandatory pension contribution rates during the current parliamentary term.

Separate research from Scottish Widows found that 2.3 million workers are currently on course to face poverty during retirement.

The bank has urged ministers to increase the combined minimum pension contribution rate from eight per cent to 12 per cent.

Scottish Widows said the proposed increase could reduce the proportion of workers heading towards inadequate retirement income from 24 per cent to 17 per cent, potentially improving outcomes for around 700,000 people.

Pension specialists have repeatedly argued that the current automatic enrolment minimum contribution rates are too low to provide millions of workers with sufficient retirement income.

The FCA figures also showed that close to 50,000 savers withdrew pension pots worth £30,000 or more in a single transaction during 2024-25.

Tom Selby, director of public policy at investment platform AJ Bell, warned savers to consider the long-term implications before withdrawing their pensions entirely.

He said: "Anyone considering cashing in their entire pension pot needs to think carefully about the tax consequences of that decision and the implications it could have for their retirement.

"Crucially, if you are taking money out of a pension and simply shoving it in a bank account, the money will be moving from an environment where it can grow tax-free to one where it could be subject to tax, while inflation will eat away at its real value over the long term."

Mr Cole said the trend also reflected wider changes in retirement provision across the workforce, with fewer employees now covered by guaranteed defined benefit pension schemes.

He said increasing numbers of workers instead rely on defined-contribution pensions, where retirement income depends entirely on the level of savings accumulated over time.