A common pension mistake could cost those approaching retirement up to nearly £50,000, as experts urge Britons to double-check whether it is worth accessing their savings as a lump sum.

Nearly half of all defined contribution pension pots accessed for the first time during 2024-2025 were withdrawn as complete lump sums, according to the Pensions Commission's interim report.

The findings show that 48 per cent of savers chose to take their entire pension in one go, prompting warnings from financial experts about the potential long-term consequences.

Antonia Medlicott, who founded and runs financial education firm Investing Insiders, has cautioned that this approach can significantly disadvantage retirees in their later years.

She explained: "Whether or not cashing out your pension is the right move varies dramatically depending on personal circumstances."

Britons are being warned about a potential pension mistake

|GETTY

For smaller pots with alternative retirement income sources, taking everything at once may be straightforward, but larger sums require more careful consideration around tax efficiency and long-term sustainability.

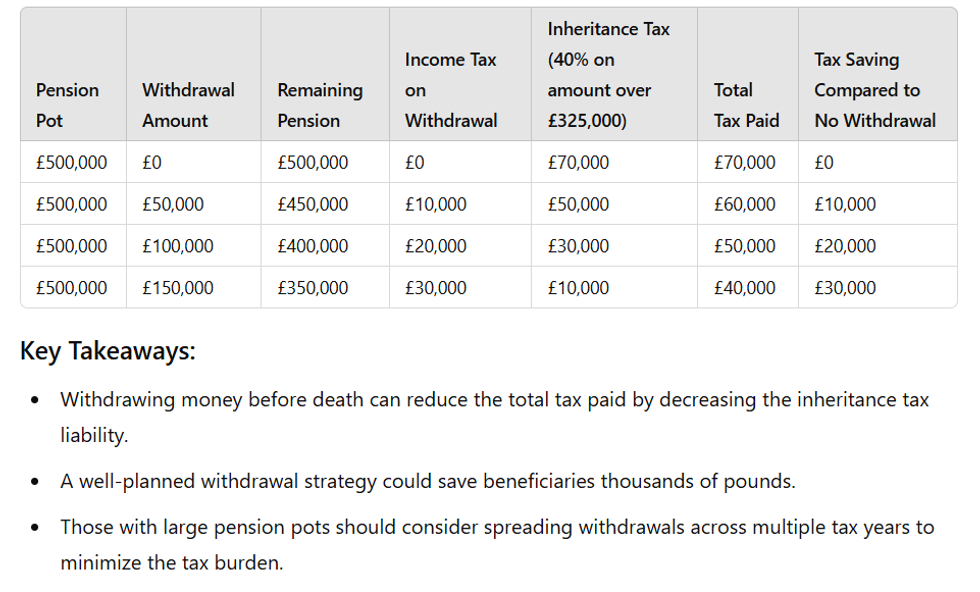

To illustrate the financial impact, Medlicott compared two approaches using a £100,000 pension pot, combined with the full state pension of £12,548 annually and £7,358 from personal savings to achieve a roughly £20,000 yearly income.

She said: "In the first scenario, you take the full £100,000 from your pension in a single tax year. You can take the first 25 per cent tax-free, leaving you with £75,000 in taxable income."

With the state pension consuming most of the £12,570 personal allowance, the entire taxable portion attracts income tax at 20 per cent on £37,700 and 40 per cent on the remaining £37,278.

The 2025/26 financial year already recorded £30.6 million in outstanding pension contributions | LIQUIATIONCENTRE

The 2025/26 financial year already recorded £30.6 million in outstanding pension contributions | LIQUIATIONCENTRELATEST DEVELOPMENTS

Workplace pension pots are being forgotten | GETTY

Workplace pension pots are being forgotten | GETTYThis creates an immediate tax liability of £22,451 on day one of retirement. Under phased drawdown, however, annual withdrawals of £7,358 generate just £1,099 in yearly tax, allowing the pension to sustain income for a full two decades.

The contrast between these strategies becomes stark when examining longevity: the lump sum approach depletes funds six years sooner than phased withdrawals.

Ms Medicott noted: "When it comes to the total tax paid, option A both pays slightly more tax and runs out six years earlier, making it a much harder sell.

"The £22,451 that you have to pay in tax on day one would've turned into £49,193 if it had stayed invested in a four per cent growth pension, showcasing the real cost of cashing out."

How much you could save by withdrawing money from your pension | GBN

How much you could save by withdrawing money from your pension | GBNThe remaining £77,549 from a full withdrawal, invested in ISAs at 4 per cent growth, would last just 14 years when drawing the annual top-up.

Notably, the Pensions Commission report also revealed the motivations behind these decisions, with 46 per cent of those cashing out using the money for significant one-off purchases such as holidays or vehicles.

Meanwhile, 27 per cent transferred their funds into current or savings accounts, prioritising accessibility over investment returns, while 23 per cent directed the money towards clearing debts.

Ms Medlicott warned that pensions are being treated "like a pot of money, akin to a savings account," resulting in high early retirement income that rapidly diminishes.