Pensioners purchasing annuities are now recovering their initial investment seven years sooner than they would have done five years ago.

A typical 65-year-old investing £100,000 in an annuity can now break even after 14 years, data from Canada Life shows.

In 2021, the same investment would have taken 21 years to return its original value.

The improvement follows a sharp rise in annuity rates, which reached their highest level in 17 years during 2025.

TRENDING

Stories

Videos

Your Say

A healthy 65-year-old investing £100,000 into a single-life annuity now receives £7,373 per year.

This compares with £4,662 five years earlier, reducing the break-even period by around one third.

The increase in returns has been driven by higher interest rates over the past three years.

Rising rates have pushed up yields on British Government bonds, with annuity pricing closely linked to gilt performance.

Pensioners break even sooner as returns hit 17-year high

|GETTY

Across the market, the average annual annuity income reached £3,558 last month.

This represents an increase of £60 compared with March 2025, according to Moneyfacts.

Demand for annuities has also increased alongside improved rates.

Financial Conduct Authority (FCA) data shows annuity sales rose 29 per cent between 2021-22 and 2024-25.

LATEST DEVELOPMENTS

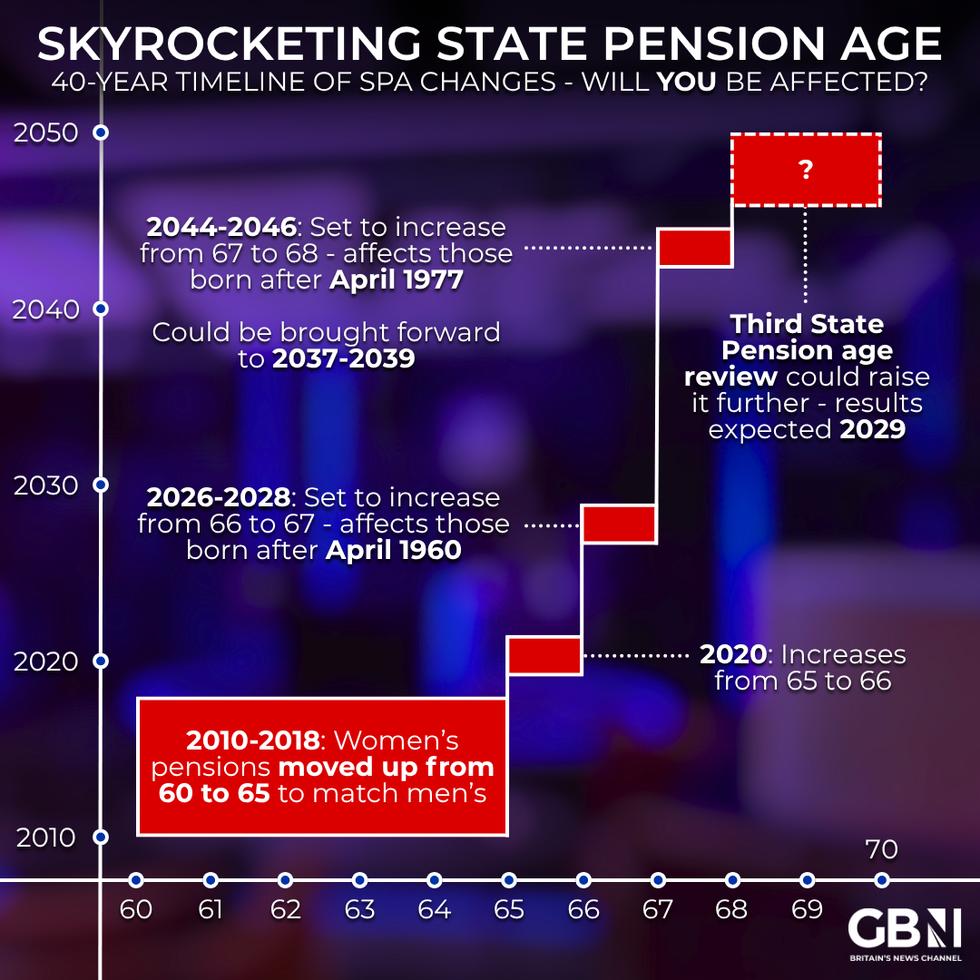

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYThe number of pension pots converted into annuities at first access increased from 68,514 in 2021-22 to 88,430 in 2024-25.

Annuities provide a guaranteed income for life, with options available for payments to rise in line with inflation.

Policy changes have also contributed to renewed interest.

Labour has confirmed that unspent pension savings will fall within the scope of inheritance tax from April 2027.

This has prompted some retirees to consider annuities as part of estate planning.

Money used to purchase an annuity is removed from a pension pot, meaning it no longer forms part of an individual’s estate for inheritance tax purposes.

This can reduce the overall value of an estate and the potential tax liability for beneficiaries.

Nick Flynn, retirement income director at Canada Life, said: "Attractive pricing and the certainty of a guaranteed income for life are increasingly valuable as people live longer and face extended retirements, making annuities a strong choice for those seeking financial stability and peace of mind."

A 65-year-old woman can expect to live a further 23 years on average

|GETTY

Rachel Springall, finance expert at Moneyfacts, said: "Higher interest rates and higher gilt yields have pushed up annuity incomes, making them more attractive to retirement savers than they were even just a few years ago."

She added: "The case to take one out has become even stronger now, particularly as unused pension pots will fall under inheritance from April 2027.

"Using part of a pension to buy an annuity can reduce the value of an estate, which means someone's bereaved relatives would pay less inheritance tax."

Office for National Statistics (ONS) data shows a 65-year-old woman can expect to live a further 23 years on average.

Men of the same age are expected to live for around 20 more years.