Yorkshire Building Society has issued an update about "lower mortgage rates" in 2026 as the lender predicts that approximately 390,324 first-time buyers secured mortgages across the UK during 2025, representing a rise of nearly a fifth compared with the previous year.

The 18 per cent jump brings the figure close to the recent high of 405,250 recorded in 2022, a year influenced by trends emerging from the coronavirus pandemic.

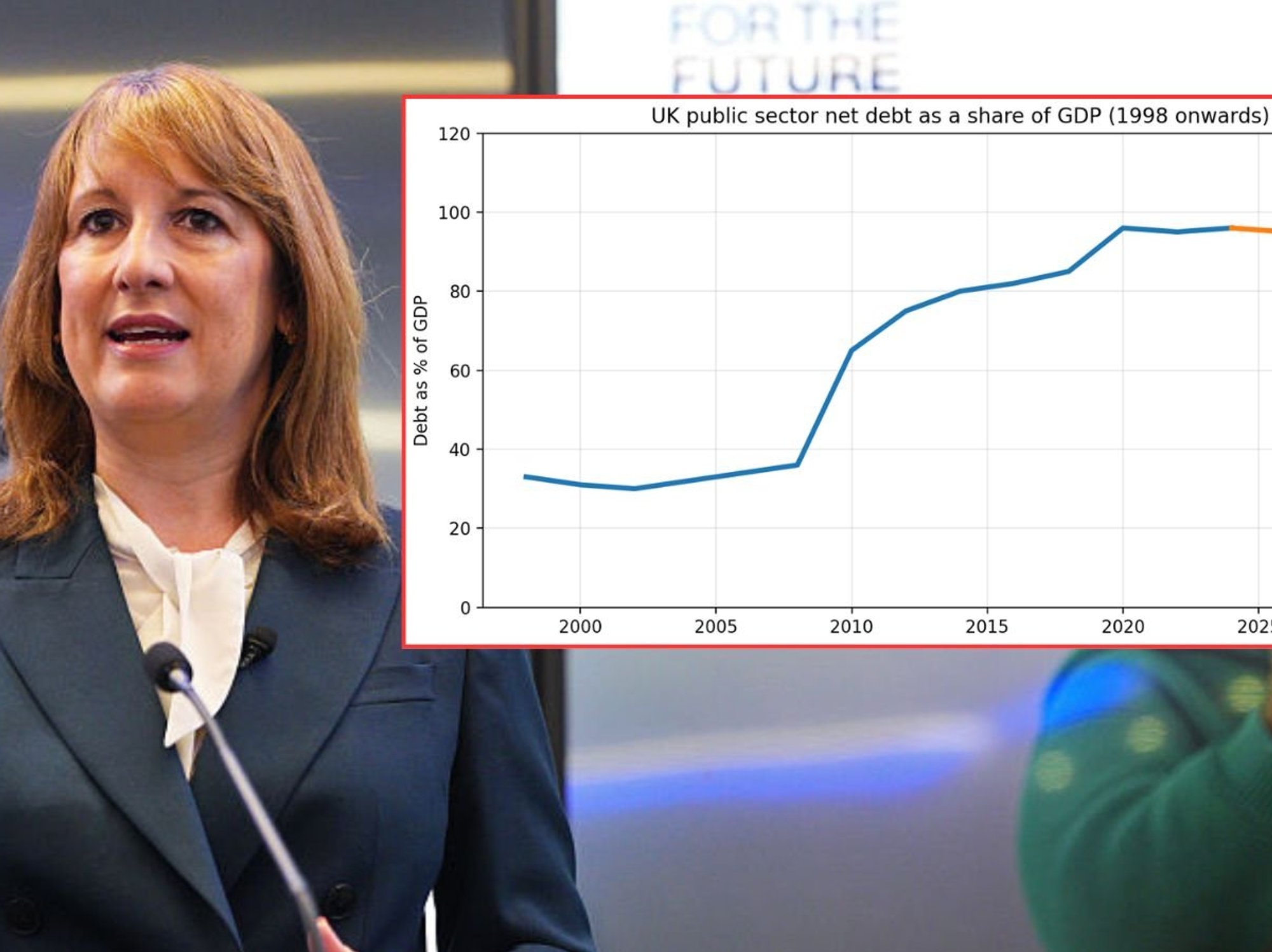

The building society based its 2025 calculations on UK Finance mortgage completion figures through to the end of October, with November and December projections derived from historical first-time buyer purchasing patterns.

According to the lender, enhanced affordability stemming from regulatory adjustments, sector innovation and declining interest rates drove the increase.

Yorkshire Building Society predicts a flurry of young homebuyers getting on the property ladder in 2026

|GETTY / PA

Max Shepherd, the group economist for Yorkshire Building Society, said first-time buyers had shown "remarkable resilience" in recent years despite various barriers to getting on the property ladder.

He added: "Tailwinds like real earnings growth, lower mortgage rates, and regulatory changes allowing lenders to lend borrowers more times their income are helping more people onto the ladder."

However, Mr Shepherd cautioned that progress must continue, noting that many prospective homeowners still face difficulties accumulating deposits or passing affordability assessments.

"We don't want to see a growing divide between the 'haves' and 'have-nots' when it comes to homeownership," he warned.

The Bank of England base rate has fallen | CHAT GPT

The Bank of England base rate has fallen | CHAT GPT Notably, the economist emphasised the significance of homeownership aspirations for many people whilst acknowledging persistent barriers remain for would-be buyers.

The broader mortgage market also experienced substantial growth, with total house purchases completed using mortgages projected to reach 717,588 in 2025, up 16 per cent from 619,120 the year before.

First-time buyers accounted for roughly 54 per cent of all mortgage transactions, making them the primary driver of this expansion.

Meanwhile, the Financial Conduct Authority (FCA) announced in December its intention to shape "the mortgage market of the future," adapting to technological advances, shifting employment patterns and evolving demographic needs.

The regulator's modernisation proposals target several key areas: supporting first-time buyers and underserved customers, addressing later-life lending, encouraging innovation in disclosure practices, and strengthening protections for vulnerable borrowers.

Mortgage holders and prospective homebuyers have been saddled with historically high interest repayments as of late due to recent decisions from the Bank of England.

The central bank's Monetary Policy Committee (MPC) has voted to raise the base rate to as high as 5.25 per cent in an effort to bring down inflation following the Covid-19 pandemic.

As inflationary pressures have eased, the Bank's rate-setters have slashed the cost of borrowing to 3.75 per cent which is expected to be soon reflected in the deals offered by lenders.

Yorkshire Building Society is sharing its forecasts for the mortgage market

| YORKSHIRE BUILDING SOCIETYAdam French, the head of News at Moneyfactscompare, said: "If the Bank of England Base Rate settles around 3.5 per cent in 2026, as current forecasts suggest, that may represent a more ‘neutral’ interest rate environment. However, what it means for households is varied.

"Mortgage borrowers may see more tangible savings, but expectations should remain measured. Over the past few years, average mortgage rates have typically sat around 0.8 percentage points above the base rate.

"On that basis, a three-3.5 per cent base rate suggests average mortgage rates settling between four per cent and 4.5 per cent, lower than today, but still substantially higher than the ultra-cheap borrowing many households became accustomed to in the 2010s.

"There are signs that uncertainty has eased since the Budget, and markets expect a further Base Rate cut to feed through into mortgage pricing. However, the outlook remains finely balanced."

More From GB News