Young people in Britain face the prospect of losing nearly £70,000 in state pension payments over their retirement years, fresh research from wealth management firm Rathbones has revealed.

The analysis highlights how Generation Z stands to be significantly worse off as the state pension age climbs to 68, with those currently aged 25 potentially missing out on up to £69,900 compared to what they would receive if the retirement age stayed at 66.

Meanwhile, middle-aged workers are also affected, with 45-year-olds set to forgo around £42,700 under the same projections.

The findings underscore growing concerns about retirement security for younger generations, who already contend with elevated housing costs, student debt burdens and broader cost of living pressures.

New research suggests future generations will be worse-off due to the state pension age rising

|GETTY

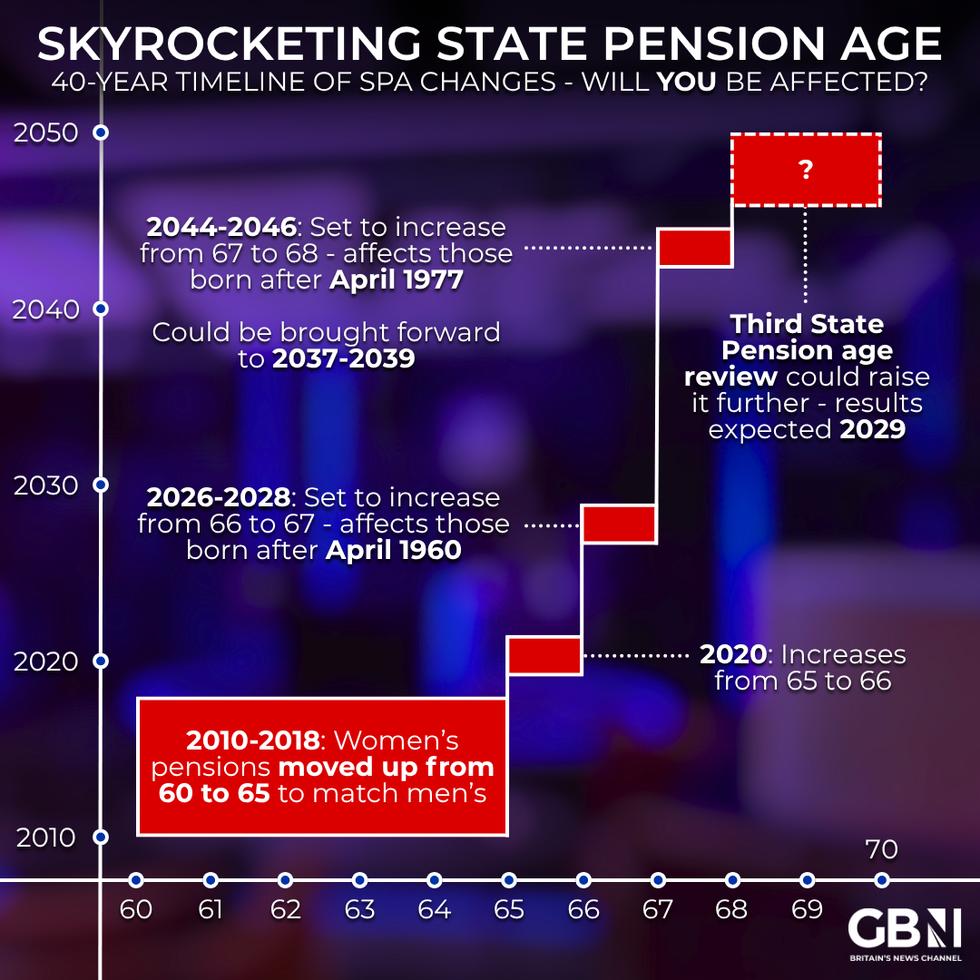

The state pension age is presently rising from 66 to 67, a transition taking place between April 2026 and April 2028.

A subsequent increase to 68 is scheduled for the period between 2044 and 2046, though a government review currently underway may accelerate this timetable.

For today's 25-year-olds, these changes could translate into forfeiting up to two complete years of state pension payments.

Rathbones based its calculations on the new full state pension rate of £12,548 annually, with increases applied at 2.5 per cent each year under the triple lock mechanism.

Are you affected by state pension age changes? | GBN

Are you affected by state pension age changes? | GBNLATEST DEVELOPMENTS

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL The financial demands of a comfortable retirement grow substantially steeper for younger savers, according to the Rathbones modelling.

A single person aged 25 today would require approximately £1.68million in savings to retire at 65, while couples in the same age bracket would need around £1.86million.

These projections assume 40 years of inflation-linked growth at two per cent before retirement and factor in state pension provision.

Should the state pension be removed from calculations entirely, the required sums jump dramatically to £2.42million for individuals and £3.35million for couples.

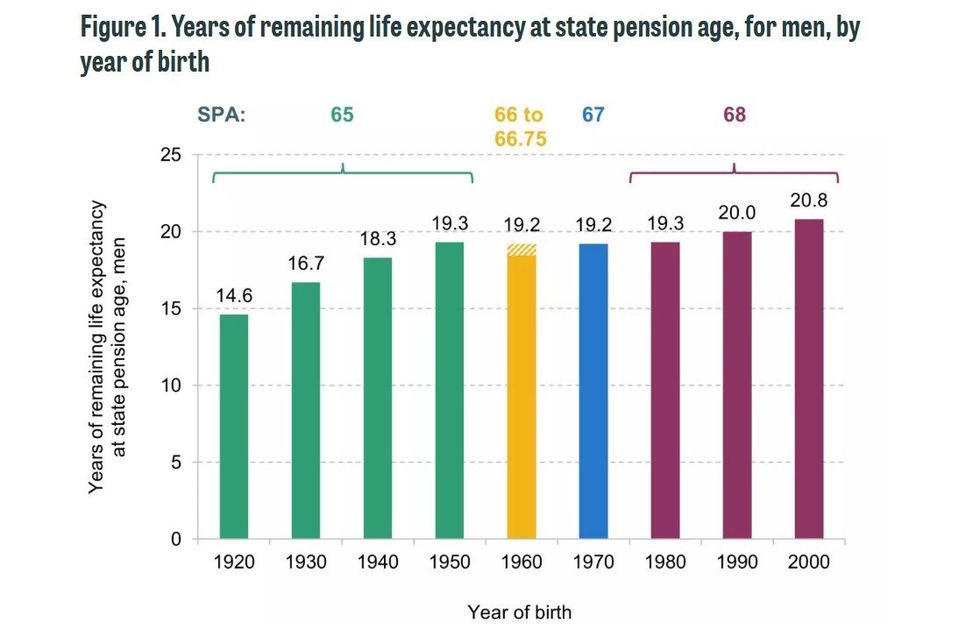

How long will you have left to life after reaching the state pension age? | IFS

How long will you have left to life after reaching the state pension age? | IFS The savings burden eases as retirement draws nearer, with 30-year-olds needing roughly £1.54million and 60-year-olds requiring approximately £885,000. Someone retiring today at 65 would need around £796,000 as a single person or £913,000 as a couple.

Ed Wood, financial planning director at Rathbones, said: "The elephant in the room for younger generations is that they are likely to face a less generous state pension system than many retirees enjoy today, pushing the bar much higher for what they need to save themselves."

He noted that many young adults now request retirement planning based on a worst-case scenario of receiving no state pension at all.

The Institute for Fiscal Studies (IFS) has warned the triple lock could cost up to £40 billion annually by 2050, raising serious questions about its long-term sustainability.