The Tony Blair Institute for Global Change has unveiled a radical blueprint to abolish the triple lock and introduce an entirely new pension framework called the "Lifespan Fund".

Under the proposed system, which some analysts are calling "dystopian", workers would build up a contributory account through employment, education, caring responsibilities, and other credited activities over four decades.

After 40 years of contributions, individuals would accumulate a maximum pot worth approximately £250,000 in current terms, providing roughly £12,500 annually for two decades of retirement.

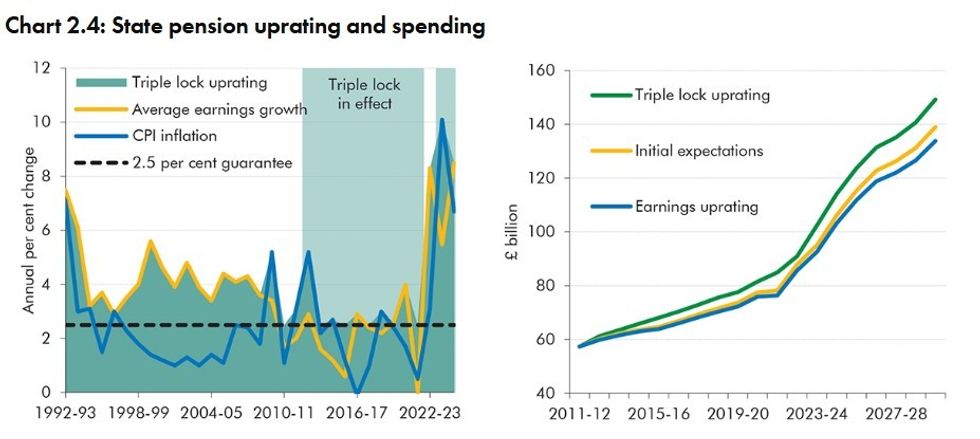

The think tank's fiscal modelling suggests this overhaul would stabilise pension expenditure at around 5.5 per cent of gross domestic product (GDP) by 2070, compared with the 7.8 per cent currently forecast. This represents potential savings of roughly £66billion each year.

A proposal by the Tony Blair Institute is calling for the state pension triple lock to be axed

|GETTY

Rather than the triple lock's guarantee of the highest of earnings, inflation or 2.5 per cent, pensions would instead follow a "smoothed earnings link" ensuring payments track wages without exceeding them.

According to Office for Budget Responsibility (OBR) projections, state pension costs will climb from their current level of five per cent of GDP to 7.8 per cent by 2070.

The TBI translates this increase as exceeding £85billion annually in today's money. To illustrate the scale of this burden, the report notes that covering such costs would demand either raising VAT from 20 to 29 per cent or slashing the health budget by nearly 40 per cent.

The triple lock mechanism, introduced in 2010 to restore pension values following decades of erosion, has become what the institute describes as "a long-run cost escalator."

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL

How the state pension triple lock has changed over the years | GB NEWS / FIDELITY INTERNATIONAL LATEST DEVELOPMENTS

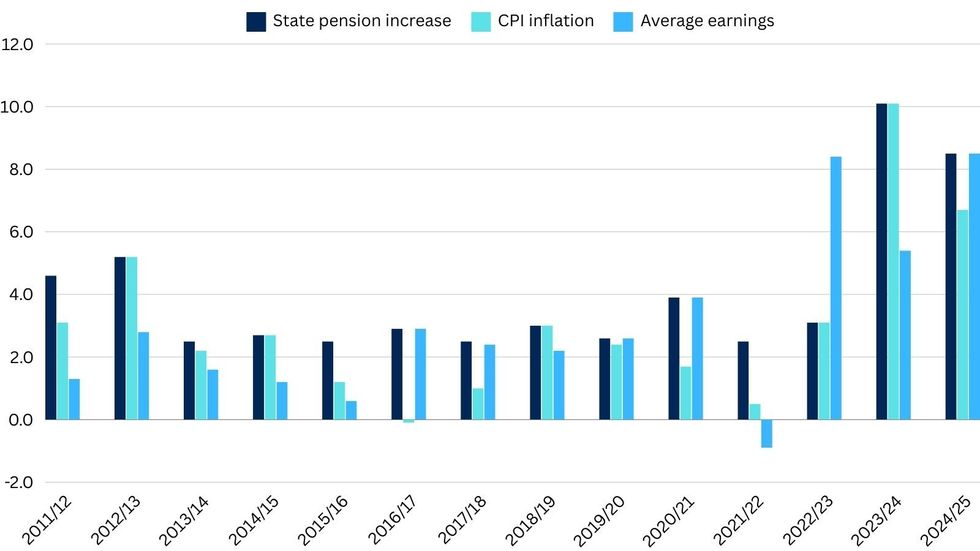

House of Commons Library data shows how the state pension has increased since 2011/12 | GB NEWS | House of Commons Library data

House of Commons Library data shows how the state pension has increased since 2011/12 | GB NEWS | House of Commons Library dataShould it remain in place indefinitely, the new state pension could reach 38 per cent of median earnings by 2070, delivering British pensioners more generous provision than their OECD counterparts but at substantial public expense.

The Lifespan Fund would introduce personalised retirement income calculations based on an individual's age and health status, functioning similarly to an annuity.

Someone with poorer health and reduced life expectancy could choose to retire earlier while receiving the same lifetime value as a healthier colleague who works longer.

A 65-year-old in good health projected to live until 95 would receive approximately half the annual income of someone with mediocre health expected to live only to 80.

How much is the state pension triple lock? | ONS

How much is the state pension triple lock? | ONS Tom Selby, director of public policy at AJ Bell, said: "The prospect of the Government calculating an 'actuarially fair' retirement income for each individual based on key details like their personal health records feels somewhat dystopian, and would clearly be vulnerable to people gaming the system by over-stating ill-health and habits like drinking and smoking.

Mr Selby highlighted the contrast with existing arrangements, noting that the current state pension is "relatively simple" compared to the TBI's blueprint.

Moving from a single-tier benefit to a flexible system would create "fiendish complexity," he warned, both for individuals navigating the new framework and for managing the transition from current arrangements.

He also cautioned that another major overhaul, coming just a decade after the last radical pension reform, could generate additional uncertainty alongside the complexity.