Over 50s are "sleepwalking" into a pension disaster as Britons considered to be in Generation X face "less financial security" than their parents once did, damning new research has found.

Gen X, those born between 1965 and 1980, are drifting towards an insufficient retirement, fresh analysis from wealth management firm Rathbones reveals.

Those born between 1965 and 1980 are significantly more likely to hold buy-to-let properties than their older counterparts, with 17 per cent owning rental homes compared to just 9 per cent of Baby Boomers.

A survey of more than 3,000 UK adults conducted by Rathbones found that despite greater property exposure, Gen Xers lag behind Baby Boomers in holding tax-efficient savings vehicles.

New research suggests over 50s are 'sleepwalking' into pension disaster as Gen X face 'less financial security'

|GETTY

The Pensions Commission's latest interim report has flagged this generation as among the most vulnerable when it comes to retirement preparedness.

Their predicament stems from unfortunate timing: many began their careers as employers were winding down defined benefit pension schemes, yet they entered the workforce too early to benefit from automatic enrolment policies that later encouraged consistent saving habits.

Furthermore, the Rathbones survey highlights a stark gap in tax-efficient holdings. The Rathbones survey highlights a stark gap in tax-efficient holdings.

Rebecca Williams, financial planning divisional lead at Rathbones, says: "Many Gen Xers are sleepwalking into retirement with far less financial security than their parents.

Britons are struggling in retirement | GETTY

Britons are struggling in retirement | GETTY LATEST DEVELOPMENTS

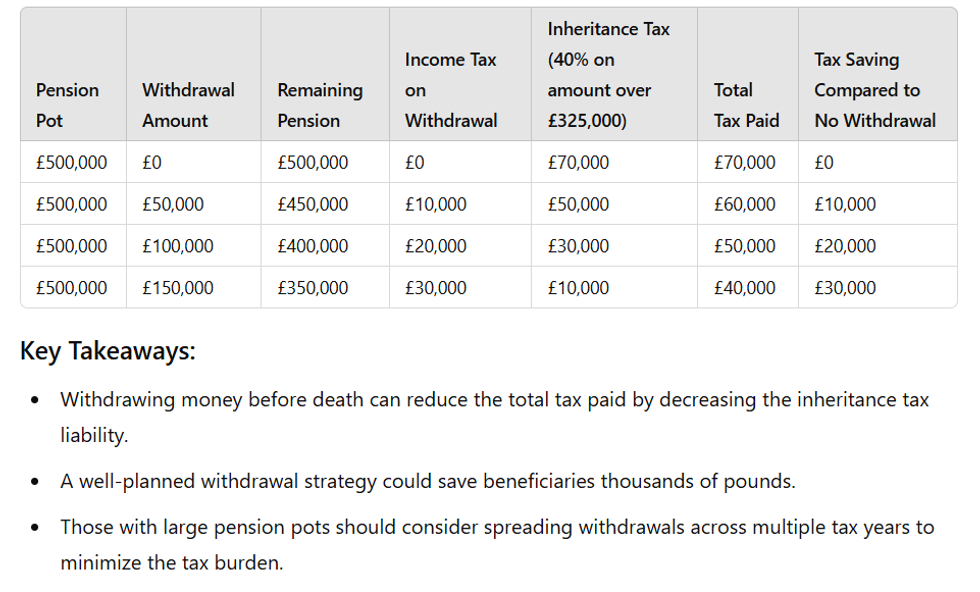

How much you could save by withdrawing money from your pension | GBN

How much you could save by withdrawing money from your pension | GBN"They came of age as defined benefit pensions were disappearing and have since faced years of stagnant wage growth and repeated financial shocks, making it harder to build robust, long-term savings."

Ms Williams notes that this cohort forms a substantial portion of the so-called sandwich generation, simultaneously supporting elderly parents and children whilst managing everyday expenses.

She added: "It's perhaps no surprise that property - particularly buy-to-let - has been seen as an alternative route to funding retirement. But relying on property as a pension can leave retirees overly exposed to a single, illiquid asset at a time when flexibility is most needed."

The conditions that propelled property values upward for decades have fundamentally altered, Rathbones' research indicates. Between 1980 and 2016, UK house prices climbed approximately 6.7 per cent annually, with London achieving 8.5 per cent.

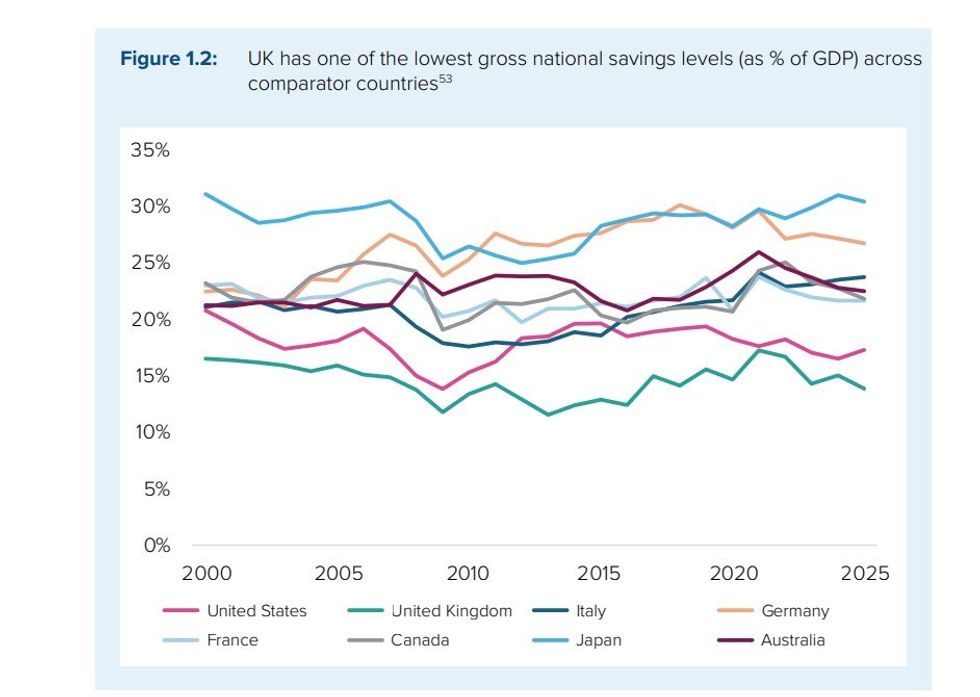

The UK has one of the lowest gross national savings levels per GDP across similar countries

|SECOND PENSIONS COMMISSION / GOV

Since 2016, however, national prices have risen just 3.7 per cent per year, whilst the capital has managed only 1.3 per cent growth. Stock market returns have vastly outstripped bricks and mortar over this period.

A £100 investment in London property in 2016 would now be worth roughly £111, whereas the same sum in equities would have grown to £174.

Isabella Galliers-Pratt, Senior Investment Director at Rathbones, says: "The idea that property is always a 'safe bet' no longer holds true in many parts of the country.

"By contrast, pensions benefit from upfront tax relief, tax‑efficient growth and access to diversified investments, making them a more structured and effective way to build long‑term retirement income."