Taxpayers can now claim money back on private pension contributions directly through HM Revenue and Custom's (HMRC) website following the launch of a new online system.

The tax authority has introduced a digital service which allows individuals to report pension tax relief without completing a self‑assessment return.

It is aimed at people making additional contributions into private pensions, including self‑invested personal pensions, alongside workplace schemes.

HMRC said it aims to review claims and respond within 28 working days.

TRENDING

Stories

Videos

Your Say

The change comes as frozen income tax thresholds draw more workers into higher tax bands.

Thresholds are set to remain unchanged until April 2031, and the Office for Budget Responsibility (OBR) estimates that 4.8 million more people will pay the 40 per cent higher rate of income tax by 2031 compared with 2022.

For those earning close to £50,270, pension contributions can reduce taxable income and potentially keep earnings below the higher‑rate threshold.

Paying into a pension lowers the amount of income subject to tax, meaning workers pushed into the higher band by a pay rise may be able to offset this by increasing contributions.

HMRC launches online pension tax relief claims tool as millions face higher tax rates

|GETTY

Mike Ambery, retirement savings director at Standard Life, said salary sacrifice arrangements can provide additional benefits.

“Because contributions are made from your gross salary, salary sacrifice can reduce the amount of income taxed at 40 per cent and lower the National Insurance you pay, while boosting your pension in a tax‑efficient way,” he said.

Under salary sacrifice, contributions are taken before tax is applied.

For example, an individual earning £50,000 who receives a £5,000 pay rise would see £4,730 of that increase fall into the higher‑rate band, normally resulting in £2,062 in tax.

LATEST DEVELOPMENTS:

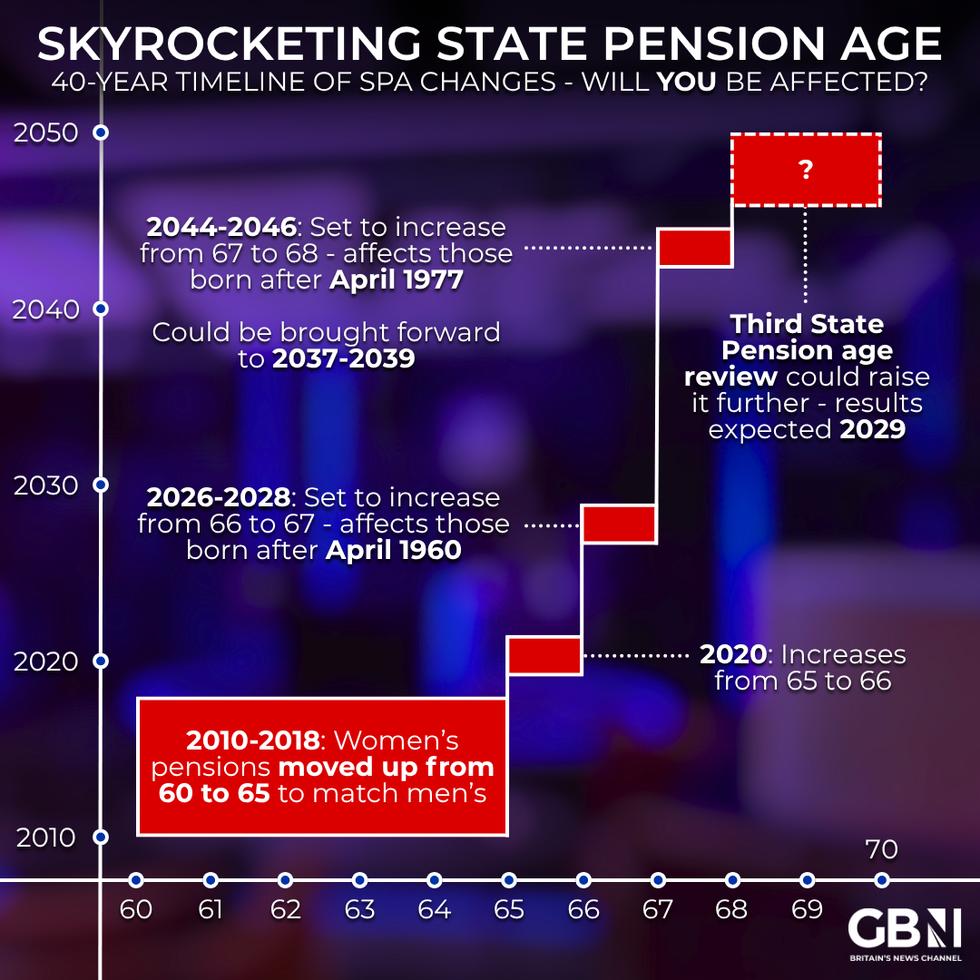

Are you affected by state pension age changes? | GETTY

Are you affected by state pension age changes? | GETTYContributing the full £5,000 into a pension through salary sacrifice may allow them to avoid higher‑rate tax on that income and reduce National Insurance contributions.

Remaining below the higher‑rate threshold can also affect other allowances. Higher‑rate taxpayers receive £500 of tax‑free interest on savings held outside ISAs, compared with £1,000 for basic‑rate taxpayers.

Crossing into the higher band can also remove eligibility for Marriage Allowance, which is worth up to £252 a year.

“A pay rise or bonus partway through the year can be enough to tip one partner into higher‑rate tax and remove your entitlement,” Mr Ambery said.

Using pension contributions to stay below the threshold may allow individuals to retain access to this allowance while increasing their retirement savings.

Financial advisers say interest in early planning has surged since the changes were announced, with many families reassessing how much of their pension they intend to leave untouched.

Wealth managers report a rise in clients seeking guidance on spending, gifting and restructuring their retirement income to limit future tax exposure.

The reforms are expected to remain a major focus for older savers over the coming year as households prepare for the new rules to take effect in April 2027.