Martin Lewis has warned pension savers about what he describes as a "massive tax trap" that could cost hundreds or even thousands of pounds when withdrawing money from their retirement pot.

The founder of Money Saving Expert highlighted the issue in guidance published on his website, cautioning taking money out in the wrong way could result in handing over between £150 and £300 in tax on a £10,000 withdrawal alone.

He said the potential losses increase proportionally for those withdrawing larger sums, meaning the financial impact can quickly escalate.

Mr Lewis explained while the mechanics of pension withdrawals appear straightforward, the structure of how funds are accessed can significantly affect the amount of tax paid.

TRENDING

Stories

Videos

Your Say

Under standard rules, when an individual takes a lump sum directly from their pension, each withdrawal is divided so that 25 per cent is tax-free and the remaining 75 per cent is subject to income tax at the person’s marginal rate.

Using a £10,000 example, £2,500 would be tax-free, while £7,500 would be added to taxable income for that year.

For a basic rate taxpayer paying 20 per cent income tax, that would mean a £1,500 tax charge on the taxable portion, while a higher rate taxpayer at 40 per cent would face a £3,000 charge.

Mr Lewis said many savers do not realise there is an alternative method which can reduce the overall tax burden, particularly for those expecting their income to fall in retirement.

Potential losses increase proportionally for those withdrawing larger sums

| ITV/THE MARTIN LEIWIS MONEY SHOW LIVE Rather than taking lump sums where each withdrawal triggers an immediate tax charge on 75 per cent of the amount, savers can instead withdraw only the 25 per cent tax-free entitlement upfront and transfer the remaining 75 per cent into an income drawdown arrangement or use it to purchase an annuity.

By doing so, the remaining funds stay invested and are only taxed at the point they are accessed in future.

Mr Lewis said: "If you take it in chunks, each withdrawal is 25 per cent tax-free and 75 per cent taxable, but there are ways to structure it so you control when you pay tax on the rest."

He explained the key advantage lies in timing, as individuals can potentially defer drawing taxable income until they fall into a lower tax bracket.

LATEST DEVELOPMENTS

That difference could amount to thousands of pounds over the course of retirement

| GETTYSomeone who is currently paying 40 per cent income tax but expects to become a basic rate taxpayer after retiring could ultimately pay 20 per cent rather than 40 per cent on the taxable portion of their pension savings.

That difference could amount to thousands of pounds over the course of retirement, particularly for those with substantial pension pots.

The same principle may apply to individuals moving from basic rate taxpayer status to becoming a non-taxpayer in later life, as deferring withdrawals could further reduce liability.

Mr Lewis warned failing to consider these options carefully could result in unnecessary tax payments that permanently reduce retirement income.

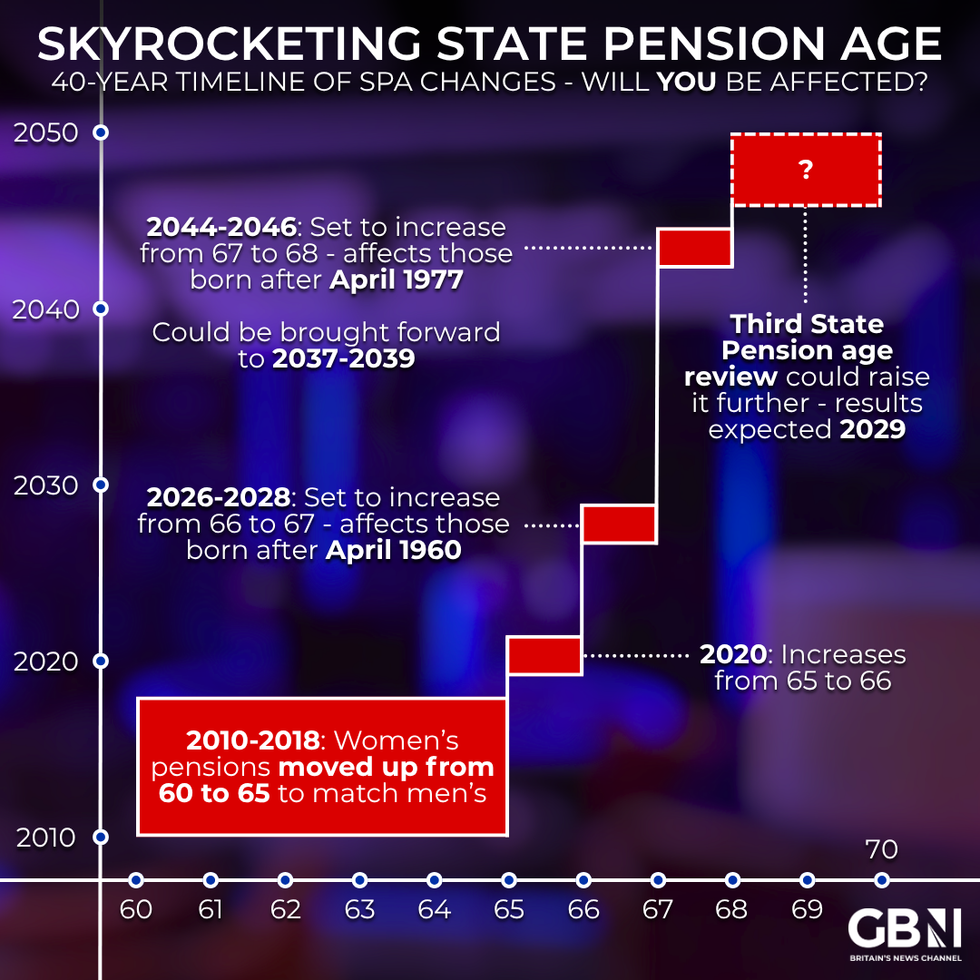

Skyrocketing state pension age - will you be affected? | GB News

Skyrocketing state pension age - will you be affected? | GB NewsHe also noted pension access rules are set to change, with the minimum age for drawing a private pension rising from 55 to 57 in April 2028.

Savers who access their pension flexibly may also trigger limits on future contributions, reducing the amount they are permitted to pay in while still receiving tax relief.

Citizens Advice recommends individuals seek guidance before making decisions about accessing personal or workplace pensions, particularly given the complexity of the rules and the potential long-term consequences.

Our Standards: The GB News Editorial Charter

More From GB News