Savers with modest amounts in fixed-rate accounts could face unexpected tax bills as HM Revenue and Customs (HMRC) begins reviewing interest earned during the 2025 to 2026 tax year.

With the tax year ending on April 5, HMRC is now assessing financial records and will issue demands to individuals who have exceeded their Personal Savings Allowance.

Banks automatically report interest earned to HMRC, meaning liabilities are calculated without the need for savers to declare the income themselves, unless funds are held within a tax-free account such as an Individual Savings Account (ISA).

Under current rules, basic-rate taxpayers earning less than £50,270 can earn up to £1,000 in savings interest tax-free.

Higher-rate taxpayers earning £50,271 or more see their allowance reduced to £500.

Those earning £125,140 or above do not receive any Personal Savings Allowance, meaning all interest is subject to tax.

The amount owed depends on total income, the level of interest earned and the timing of when that interest is paid.

Fixed-rate savings accounts can create unexpected liabilities because interest is typically paid in a single lump sum when the account matures.

HMRC issues savings tax warning as Personal Savings Allowance bills loom

| GETTYThis means the full amount is counted within one tax year rather than being spread across the duration of the account.

For example, a saver placing £3,500 into a three-year fixed-rate account at five per cent would generate more than £500 in interest, potentially exceeding the allowance in one payment.

This structure means higher-rate taxpayers could exceed their £500 threshold with relatively small balances, particularly if they hold multiple accounts.

For those paying the higher rate of income tax, any interest above the allowance is taxed at 40 per cent, compared with 20 per cent for basic-rate taxpayers.

LATEST DEVELOPMENTS

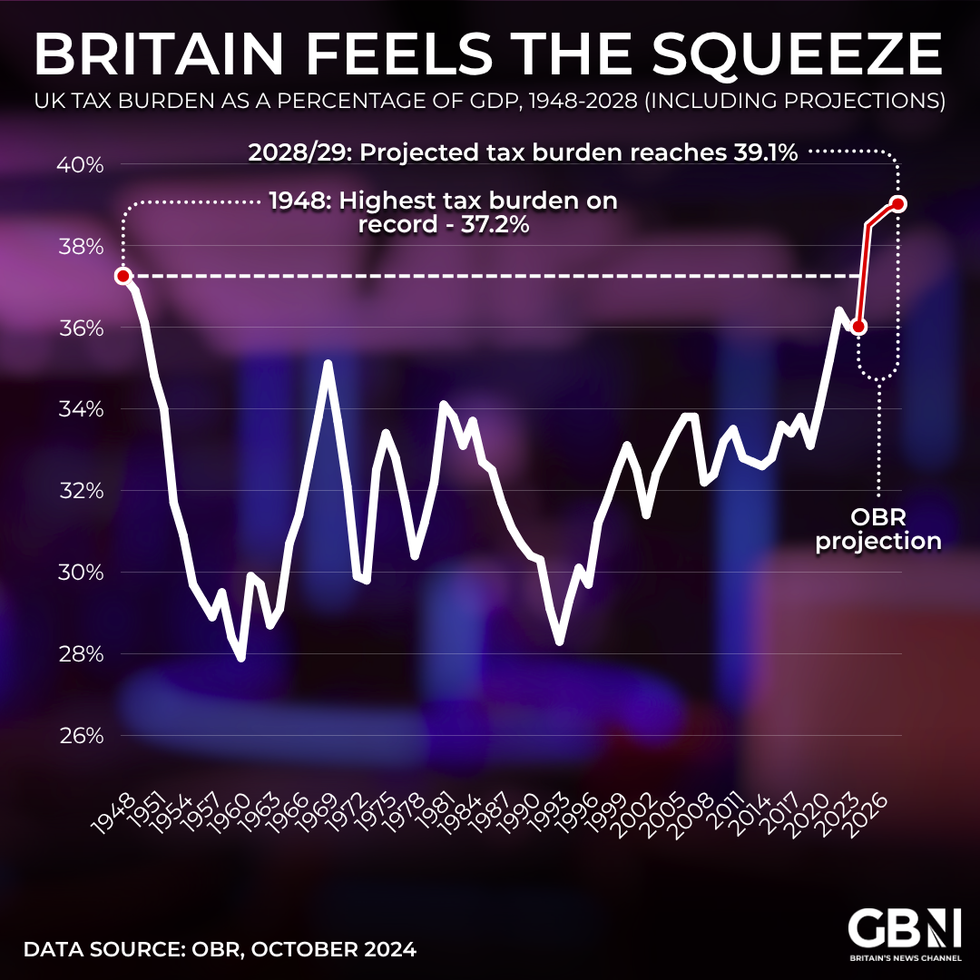

UK tax burden as a percentage of GDP | GB News

UK tax burden as a percentage of GDP | GB NewsExceeding the allowance by £100 would result in a £40 tax charge for higher-rate earners.

Even easy-access accounts can trigger liabilities, with savings of £11,000 at five per cent generating £550 in annual interest, enough to exceed the threshold for higher-rate taxpayers.

HMRC said: "If you go over your allowance, you pay tax on any interest over your allowance at your usual rate of income tax."

For individuals in employment or receiving a pension, HMRC typically collects any tax owed by adjusting their tax code automatically.